Chapter One

Understanding the role of digital financial literacy in online banking behavior

Financial activities–from paying bills to checking bank balances to sending money to friends–have increasingly moved online, making digital literacy critical to managing our finances.

“Financial literacy is key to owning our financial lives and futures,” said Adam Davis, Vice President, Financial Health, Inclusion, and Liquidity at Capital One. “But consumers increasingly say they prefer managing their finances online, so the question we should be asking is how can we help them master financial literacy in a digital environment.”

To help answer that question, a new study from the Capital One Insights Center measures consumers’ digital and financial literacy and explores the role this knowledge plays in online banking.

The survey found that most Americans (about 86%) know how to protect themselves and their personal information online, which is a major component of digital literacy. However, over 40% of consumers lack basic financial knowledge, like how to manage debt or build credit. Previous research has shown that financial literacy improves financial well-being.

The survey also found that most Americans, even those with low digital literacy, prefer and are already actively using a mobile app or website to manage their finances. These findings indicate that digital literacy is not a significant barrier to engaging with digital banking. By appealing to consumers’ stated preferences and existing behaviors, digital banking has the power to surpass the reach of traditional physical servicing channels (e.g., bank branches, ATMs and call centers), offering consumers continuous access to their finances and the opportunity to promote general financial well-being.

How Americans rate on digital financial literacy

Although financial literacy has been well studied, digital financial literacy is an emerging concept that measures the intersection of financial skills and digital safety knowledge. Online financial activities are a target for fraud and scams, so early research on digital financial literacy has emphasized the knowledge needed to safely engage online.

To gauge levels of digital financial literacy and digital banking behaviors, the Insights Center surveyed 3,000 consumers across the United States from August to September 2023.

As with previous research in the field, our survey also measured digital literacy by evaluating digital safety knowledge, like how to identify phishing scams and whether it’s safe to share personal information on private social media accounts (see the methodology section for more information).

Consistent with that past research, our measure of financial literacy focused on core financial concepts such as credit, debt and interest.

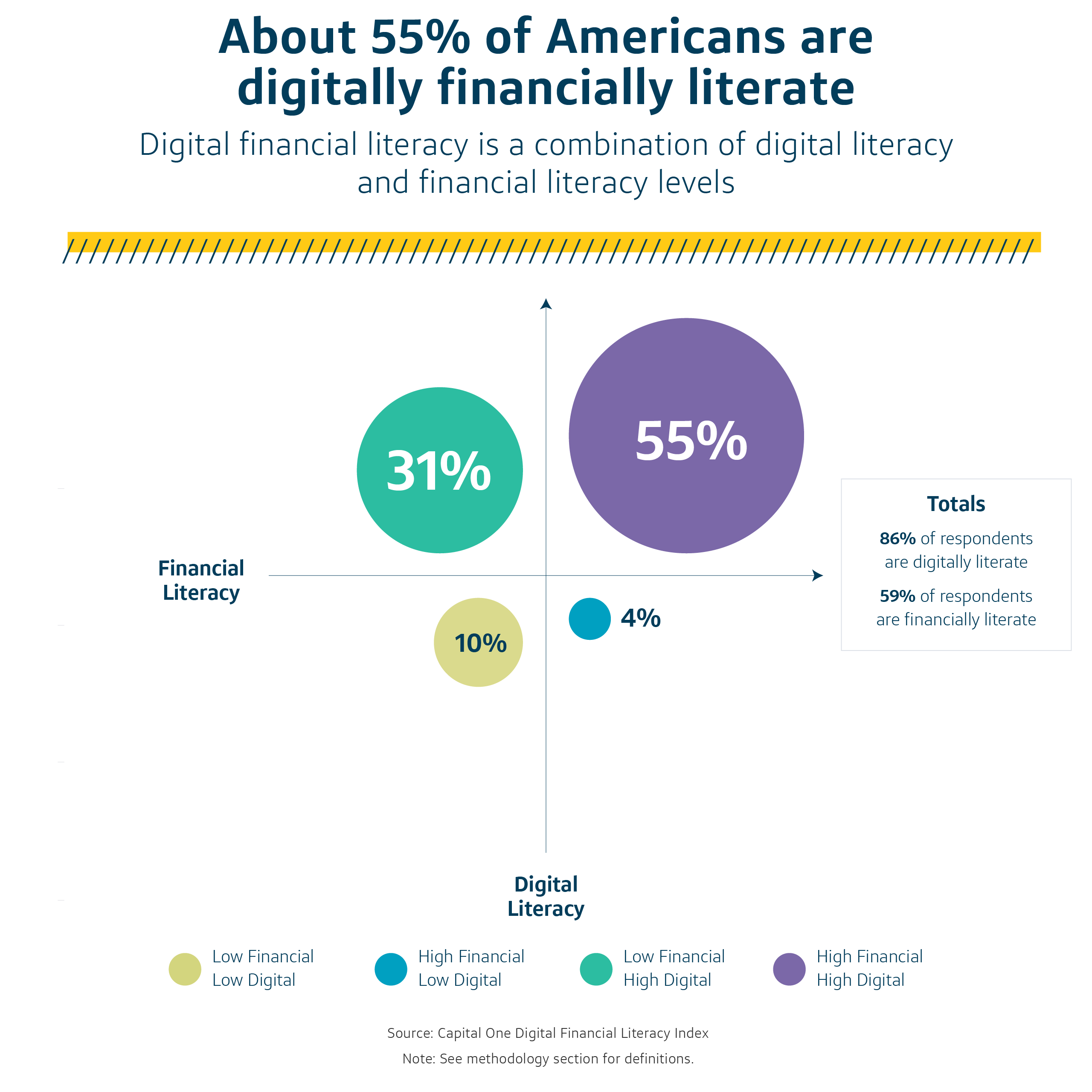

Our study showed that, overall, about 55% of Americans are digitally financially literate, meaning they scored high in both digital literacy and financial literacy.

About 86% of consumers are digitally literate: the “high financial–high digital” population (55%) plus the “low financial–high digital” population (31%).

Roughly 59% of consumers are financially literate: the “high financial–high digital” population (55%) plus the “high financial–low digital” population (4%). These findings align with previous research on financial literacy.

The survey also found that digital financial literacy increases with age. Older consumers tend to rank high in both digital and financial literacy. By contrast, younger consumers tend to score high in digital literacy but low in financial literacy.

Although younger consumers may have grown up in the digital age, they are still at risk of being scammed. However, our study indicates that younger consumers’ high digital literacy may offer an opportunity to improve their financial literacy by harnessing the digital channels they prefer, such as online education, automated reminders and just-in-time notifications.

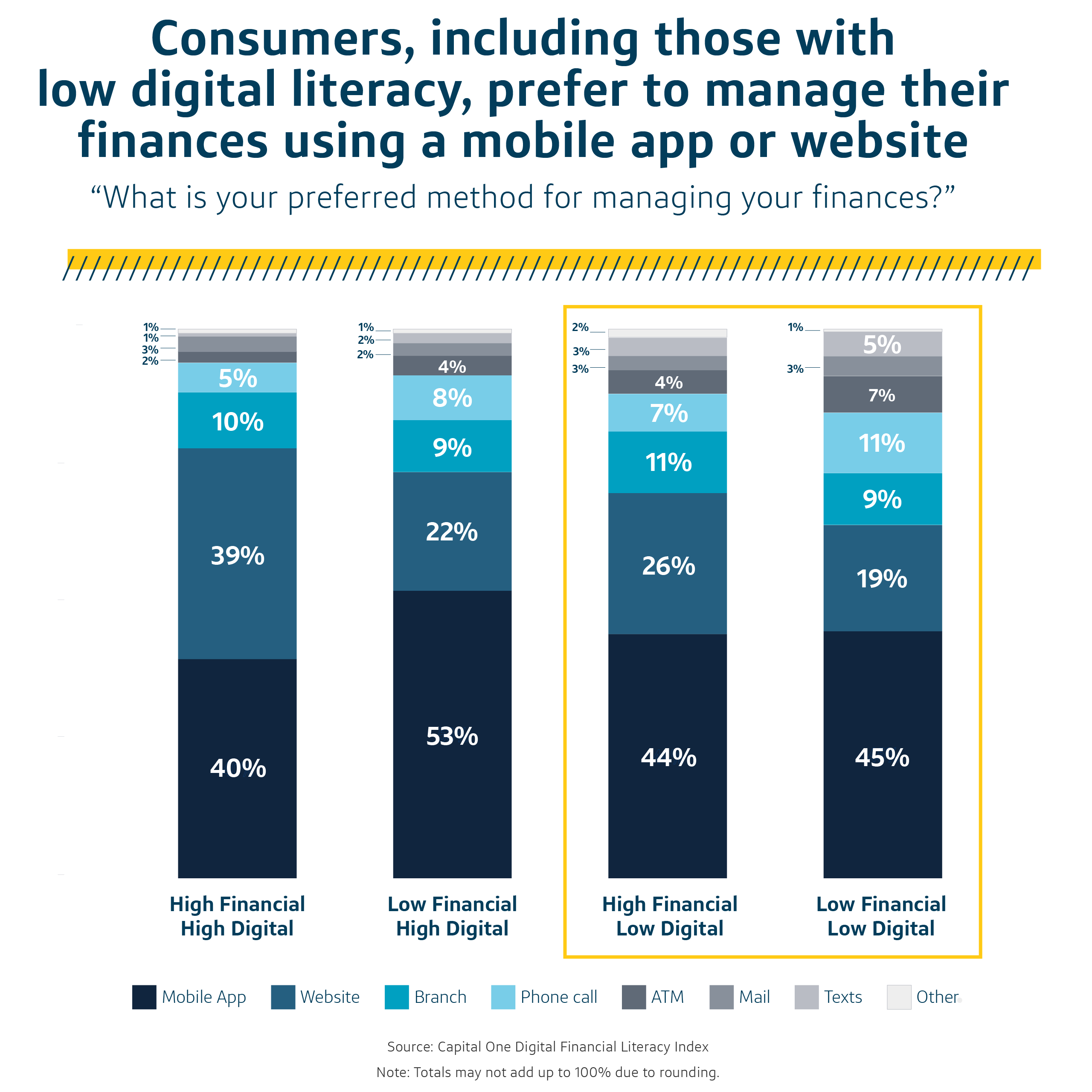

Consumers prefer to bank online, regardless of their level of digital literacy

Survey respondents overwhelmingly said they prefer to use digital channels to manage their finances. Even among consumers who scored low on both digital and financial literacy, 45% said they prefer managing their finances through a mobile app, 19% prefer using a website, and only 9% prefer going to a bank branch. Previous research shows similar behaviors.

These preferences drive home the need to ensure that consumers have basic digital financial literacy knowledge so that they’re able to manage their finances how and where they prefer. It’s also important for banks and financial services providers to continue investing in products, platforms and services that consumers can use, regardless of their level of digital literacy.

How Americans bank online

At least 7 out of 10 US households report being enrolled in digital banking for some or all of their financial accounts. To better understand how Americans bank online, we took a closer look at this group.

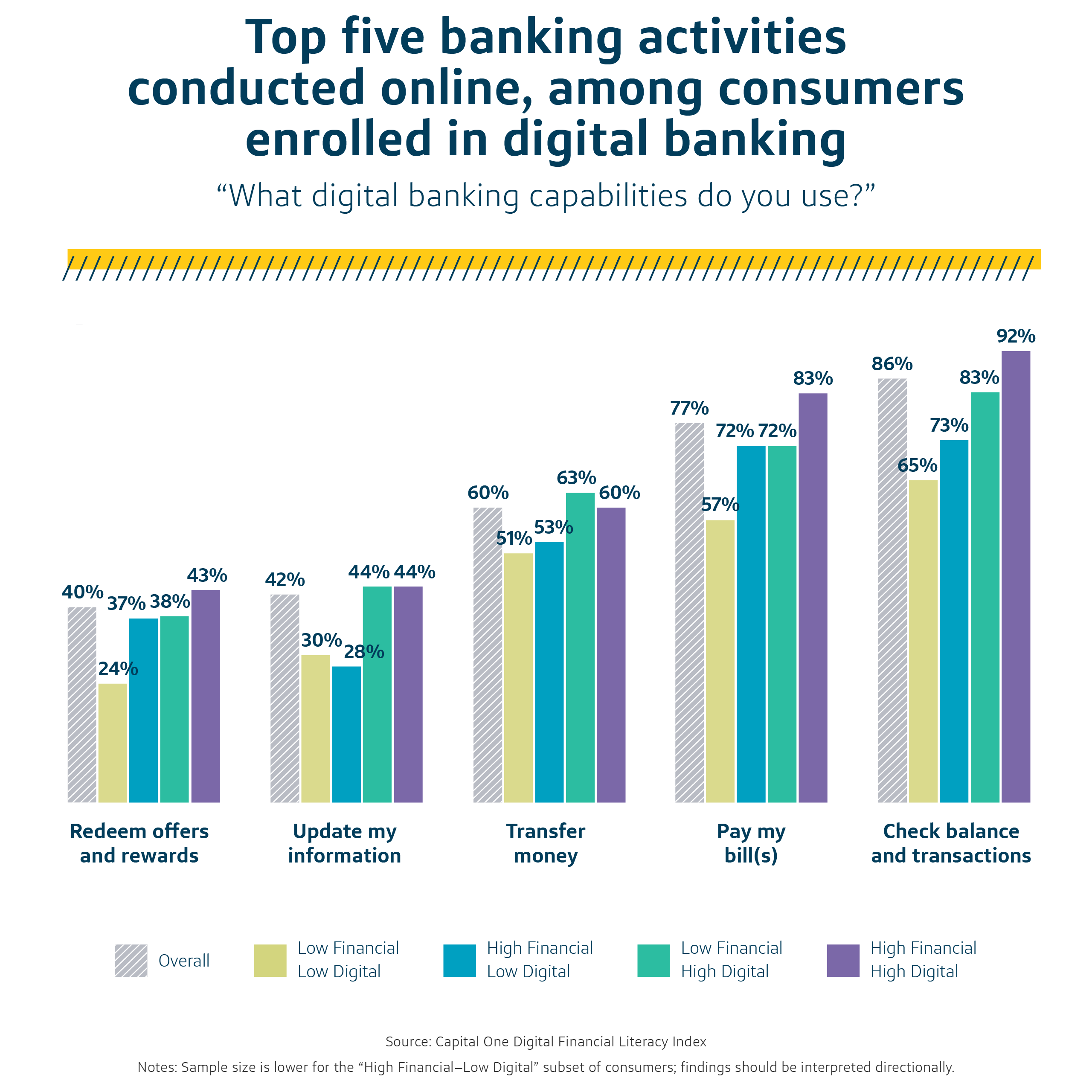

Among consumers who are enrolled in digital banking, 95% said they bank online “often” or “occasionally.” Even those with low digital literacy report that they frequently bank online.

Among those enrolled in digital banking, many consumers–even those with low digital literacy–conduct routine financial transactions online or on mobile apps. Overall, about 86% of consumers enrolled in digital banking said they check their balances and transactions digitally, 77% pay their bills digitally, and 60% transfer money digitally.

Do consumers use online financial management tools? Online financial management tools–such as tools that monitor credit scores or manage budgets and subscriptions–are designed to help consumers improve their financial health. Our study found that, among all consumers, those with low digital financial literacy are often more likely to use these online tools, perhaps indicating that they want or need help understanding and managing their finances.

Banking is digital

Digital banking surpasses the reach of traditional physical servicing channels (e.g., bank branches, ATMs and call centers) by giving consumers greater flexibility and convenience. Our research explores whether consumers have the digital literacy skills they need to take advantage of digital banking opportunities.

The Pew Research Center finds that 93% of American adults use the internet, and the gap between urban and rural Internet access is shrinking. Consumer Affairs finds that 92% of Americans have at least one smartphone, and smartphone ownership is high among urban, suburban and rural communities. Building on this research, we found that 86% of Americans, including older consumers, are digitally literate and well-equipped to use digital platforms to meet their routine banking needs.

Our findings also show widespread adoption of digital banking across demographic groups because it appeals to consumers’ expressed preferences and existing behaviors, regardless of their digital literacy levels.

These results indicate that as we move to near ubiquity in digital access and digital literacy, digital banking is effective at reaching across generations and geographies. And compared with traditional physical servicing channels, digital banking can be accessed anywhere at any time, more consistently meeting consumers’ evolving needs, circumstances and expectations.

In addition, our finding that over 40% of consumers are not financially literate suggests the need to continue investing in financial education. Many states now require high school students to take a financial education class in order to graduate.

Because consumers of all digital and financial literacy levels say they prefer managing their finances online, financial education might benefit by including lessons on how to safely and effectively engage online, especially in financial contexts.

By leaning into online platforms for learning, financial educators can meet consumers where they are. For example, Khan Academy, a leader in online learning, has partnered with Capital One to offer free online financial literacy courses. Online financial education–or a combination of digital and financial literacy training–might also attract and retain more learners.

Methodology

Capital One’s Digital Financial Literacy Index is a nationally representative, self-reported, anonymous survey of 3,000 randomly selected adults in the US. Participants were surveyed between August and September 2023.

All data in this report is from self-reported, anonymous research of U.S. consumers broadly, not specifically from or about Capital One customers or employees.

Respondents were asked a series of questions about financial literacy, digital literacy and digital banking behaviors. To measure financial literacy and digital literacy, the Insights Center used well-tested and validated questions pulled from other reputable studies.

For digital literacy, we measured the knowledge consumers need to engage online safely rather than asking about their ability to use a smartphone or computer. This focus is in line with previous research on digital financial literacy that emphasizes the need for “awareness of digital financial risks,” such as phishing and spyware; acknowledges that digital literacy goes beyond technical know-how; and defines digital literacy as possessing the skills to “meaningfully, responsibly and safely participate in the digital ecosystem.”

Also, respondents completed the survey online, which required them to have a baseline understanding of websites and/or mobile devices. Therefore, we asked more challenging questions that assumed a basic level of digital access.

About 93% of American adults use the Internet, according to the Pew Research Center. More research is needed to understand digital financial literacy among Americans who do not have access to or do not use the Internet.

Consistent with past research, our measure of financial literacy focused on core financial topics such as credit, debt and interest.

Modeling the Organisation for Economic Co-operation and Development (OECD)’s approach to measuring financial literacy, we defined a minimum target score to establish financial literacy and digital literacy. The target score was a simple majority of 4 out of 6 correct questions for each literacy index.

A respondent is considered to be digitally financially literate if they attained the minimum target score for both digital and financial literacy. The results were not weighted.

About the Capital One Insights Center

The Center combines Capital One research and partnerships to produce insights that advance equity and inclusion. As a nascent platform for data and dialogue, the Center strives to help changemakers create an inclusive society, build thriving communities and develop financial tools that enrich lives. The Center draws on Capital One’s deep market expertise and legacy of revolutionizing the credit system through the application of data, information and technology.

Disclaimer

This material has been prepared by the Capital One Insights Center, a non-partisan center for objective research and insights, and is provided solely for general information purposes. Unless otherwise specifically stated, any views, analysis or opinions expressed herein are solely those of the Capital One Insights Center’s staff, researchers and listed partners (if applicable) and may differ from the views and opinions expressed by Capital One Financial Corporation, other departments or divisions of Capital One Financial Corporation, or its affiliates and/or subsidiaries (Capital One). Information has been obtained from sources believed to be reliable.

The data relied on for this report are based on self-reported survey data from anonymous respondents across the U.S. Survey respondents included may or may not have relationships with any number of financial institutions and/or products. Capital One Insights Center does not know, nor is it able to determine, if any of the survey respondents have a relationship with Capital One. Certain information herein is also based on data obtained from third-party sources believed to be reliable.

Analysis and conclusions constitute the Capital One Insights Center’s judgment as of the date of this report and are subject to change without notice. Furthermore, the analysis and views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication.

Any opinions expressed herein should not be construed as an individual recommendation for any particular customer or client and is not intended as advice or recommendations of particular securities, financial instruments, market conditions or strategies. Capital One Financial Corporation and its affiliates and/or subsidiaries may issue reports or have opinions that are inconsistent with, and reach different conclusions from, this report.