Renting vs. buying a home: What to consider

While many people may strive to own a home, renting is a great option as well. Lifestyle, location, timing and tons of other financial factors can play a role in whether to rent or buy.

There are potential advantages and disadvantages to each. Knowing how to compare renting versus buying could help you weigh your options and make a decision that’s right for you.

Key takeaways

- Both renting and buying a home typically require a steady income to cover monthly expenses.

- Renting a home has lower upfront costs than buying one, and landlords usually handle repairs and maintenance.

- Buying a home offers stability and potential tax benefits that renting does not. Plus, homeowners might be able to build equity.

- According to the U.S. Census Bureau, 65.8% of Americans are homeowners.

Renting vs. buying a home: Advantages and disadvantages

When you compare renting versus buying a home, you may wonder which choice is right for you. Factors like your debt-to-income ratio, credit scores and the level of risk and responsibility you would like to take on could all influence that decision.

As you explore your options, here are a few things to keep in mind:

| Buying | Renting | |

| Pros |

|

|

| Cons |

|

|

Things to consider before buying a home

For many, buying a home is part of the American Dream. Rising interest rates, historically high home prices and limited inventory might make you question if it’s possible to turn that dream into reality.

These factors don’t necessarily mean you shouldn’t buy a home right now. But there are some key things to consider, including the potential benefits and drawbacks of homeownership:

Investment potential

Advantage: Owning a home can build equity, which is a property’s current value minus its existing mortgage balance. Building equity can increase a person’s assets while lowering their debt. Increasing a home’s value through renovations or paying down a mortgage are two possible ways to build equity.

Disadvantage: Owning a home is a big financial investment, and like any investment, it comes with potential risks. After all, building equity takes time and it’s not guaranteed. That’s because several factors—like real estate market changes or outdated home styles—could drive down property value.

Credit building

Advantage: Most people can’t afford to pay cash for a home, so they use a mortgage. According to Experian®, lenders typically report mortgage payments to credit bureaus every month. That’s why paying a mortgage on time, every time, could help a homeowner’s payment history and credit scores. A mortgage may also improve their credit mix.

Disadvantage: When someone applies for a mortgage, their lender will perform a hard inquiry, which can show up on their credit reports and affect their scores. Home foreclosures can also affect credit scores, and this type of activity may stay on credit reports for up to seven years.

Taxes

Advantage: Owning a home may come with tax benefits—like property tax or mortgage interest rate deductions. And homeowners who work remotely could qualify for a home office deduction.

Disadvantage: Homeowners typically have to pay property taxes, which are based on a home’s value. These tax rates can vary by state and county.

HOAs

Advantage: Homeowners association (HOA) communities may offer residents amenities, such as pools, tennis courts or golf courses. They could also have rules—like parking, noise or short-term rental restrictions—to maintain a uniform neighborhood appearance and protect property values.

Disadvantage: HOAs can have high costs that might range anywhere from $200 to $2,500 per year. And failure to follow their rules could result in a lien against the homeowner’s property.

Customization

Advantage: Homeowners typically have the freedom to make a home look and feel like their own through renovations and landscaping. Home improvement projects might even boost a home’s curb appeal and value.

Disadvantage: Neighborhoods with HOAs could have restrictions on how a homeowner can renovate or decorate their property. Homeowners cover their own renovation costs, so it’s helpful to know how any repairs or upgrades you’d like to make to a home could affect your purchasing budget.

Costs

Advantage: Buying a home has potential tax-saving benefits. And each mortgage payment a homeowner makes could help them pay down debt and build equity.

Disadvantage: Buying a home requires a down payment and closing costs, which can range anywhere from 3.5% to 20% of the sale price. And buyers who put less than 20% down typically have to pay private mortgage insurance (PMI). Home buyers are responsible for home repairs, and unplanned costs—like replacing a roof, HVAC system or septic tank—can add up quickly.

Stability

Advantage: Buying a home often means staying in one location longer, which can be a good thing for keeping children in their school district or staying in an area you love.

Disadvantage: If you want to move or need to relocate for a job, though, it could take some time to find a buyer. Owning a home might make relocation more expensive. That’s because homeowners may need to invest in upgrades or repairs before they list their house. And if they use a realtor, they’ll likely have to pay this person a commission.

Things to consider before renting

There are some potential benefits of buying a home, but it isn’t always the best decision. Depending on your current financial situation and long-term goals, it could make more sense to rent.

If you’re thinking about renting a property, you may want to keep these things in mind:

Flexibility

Advantage: Renting a home may offer more flexibility than buying one. If a renter changes jobs or wants to move to a new city, they aren’t tied down to a property. But it’s important to review the terms of a rental agreement to know how much notice a landlord expects.

Disadvantage: Renters may face less stability with their living situation than home buyers. A landlord could raise rent, end a lease agreement or sell the property on short notice. The amount of notice a landlord is required to give renters could depend on the lease agreement and the property’s location.

Less responsibility

Advantage: Property owners, not renters, are typically responsible for maintenance—like repairing leaking faucets or replacing broken appliances. Having someone else manage and pay for these services can give a renter peace of mind and save them money.

Disadvantage: A renter could have less freedom to personalize their space. Their landlord may not allow them to make changes to the property. If they hang photos on the wall or install new fixtures, they might risk losing their security deposit when they move.

Costs

Advantage: Renting a property often has lower upfront costs than buying one. Renters don’t have to worry about the costs that come with buying a house, such as a down payment, closing costs or property value changes. Because landlords usually handle repairs and maintenance, renters might have more predictable monthly expenses than homeowners.

Disadvantage: Renters generally need to pay a security deposit—often the first and last month’s rent payment—to secure a rental property. A landlord may also require them to pay for renters insurance.

Taxes

Advantage: Unlike homeowners, renters don’t pay property taxes. That’s because the landlord, or property owner, is responsible for paying these taxes.

Disadvantage: Since landlords pay property taxes, they may be eligible for tax benefits, like rental expense deductions. However, renters don’t receive these tax benefits.

Current market

Advantage: When interest rates and home prices are high, renting may be a better option.

Disadvantage: If rental prices are on the rise too, renting might not be a benefit. For example, the U.S. Bureau of Labor Statistics reported that new tenants experienced an average 12.2% increase in 2022 rent prices. And existing renters saw an average price increase of 3.5%.

How to decide whether to buy or rent a home

Choosing whether to buy or rent a home is a big financial decision, and it’s also a very personal one. The choice that’s best for you will likely depend on several factors.

Lifestyle

While you’re deciding whether to rent or buy, think about how the place you live fits into your lifestyle. Are you a homebody? If so, investing more of your budget in a house could make sense for you. But if you like to travel or hit the town often, you might not want a large rent or mortgage payment eating into your discretionary income.

You should also consider the square footage you realistically need and if you want a yard. If you live alone, a small space with minimal upkeep may be ideal. But if you have a large family and pets, you might want to look at larger properties with backyards.

Keep stability in mind, too. If your career requires frequent relocation, renting could be the better option. But if you’re looking to settle down in an area you love, it might be time to consider buying a home.

Long-term goals

If homeownership is important to you, taking steps to improve your financial health—like increasing your income, paying off debt or improving your credit scores—might help you reach your goal.

If you want to retire early and travel the world, you might prioritize saving and investing over paying off a mortgage. In this case, finding an affordable rental property with a short-term lease could be a better option.

Location

When it comes to real estate, location matters. And the area you live in—or want to live in—could seriously affect your budget and options due to the cost-of-living (COL). Some cities have a very high cost of living (HCOL). But others may have a low cost of living (LCOL).

If you work in an HCOL city but hate commuting, renting an apartment close to your office could be ideal. But if you work remotely or don’t mind driving in from a nearby suburb, buying in an LCOL town might be the way to go.

Costs

Renting doesn’t require the same upfront and long-term costs that buying does. But renters don’t have the same investment potential or tax benefits that homeowners do.

If you want to buy, consider how homeowners insurance, utilities, PMI, a down payment and closing costs could affect your budget. Consider any purchases—like new appliances, repairs or a backyard fence—you might need to make once you move, too. And don’t forget to factor property taxes and interest rates into your home-buying budget.

Renting may be cheaper than buying, but it also has set expenses you’ll need to consider. You may have to pay for renters insurance. It’s also a good idea to review your lease agreement and know which utilities you’ll be expected to cover.

Risks

Whether you rent or buy, each choice comes with its own risks. Renting is often cheaper than buying, but renting won’t help you build equity. Not having to worry about home repairs and having more flexibility might make renting worth the financial trade-off to some people.

Buying a home can be expensive, but it can also help you build equity. Remember, though, that buying a home isn’t a risk-free investment. If you finance a home at a high price and the property value declines, you could end up owing more money than the home is worth.

You could research property records in your area to see how well homes hold their value in order to get a better idea of resale potential.

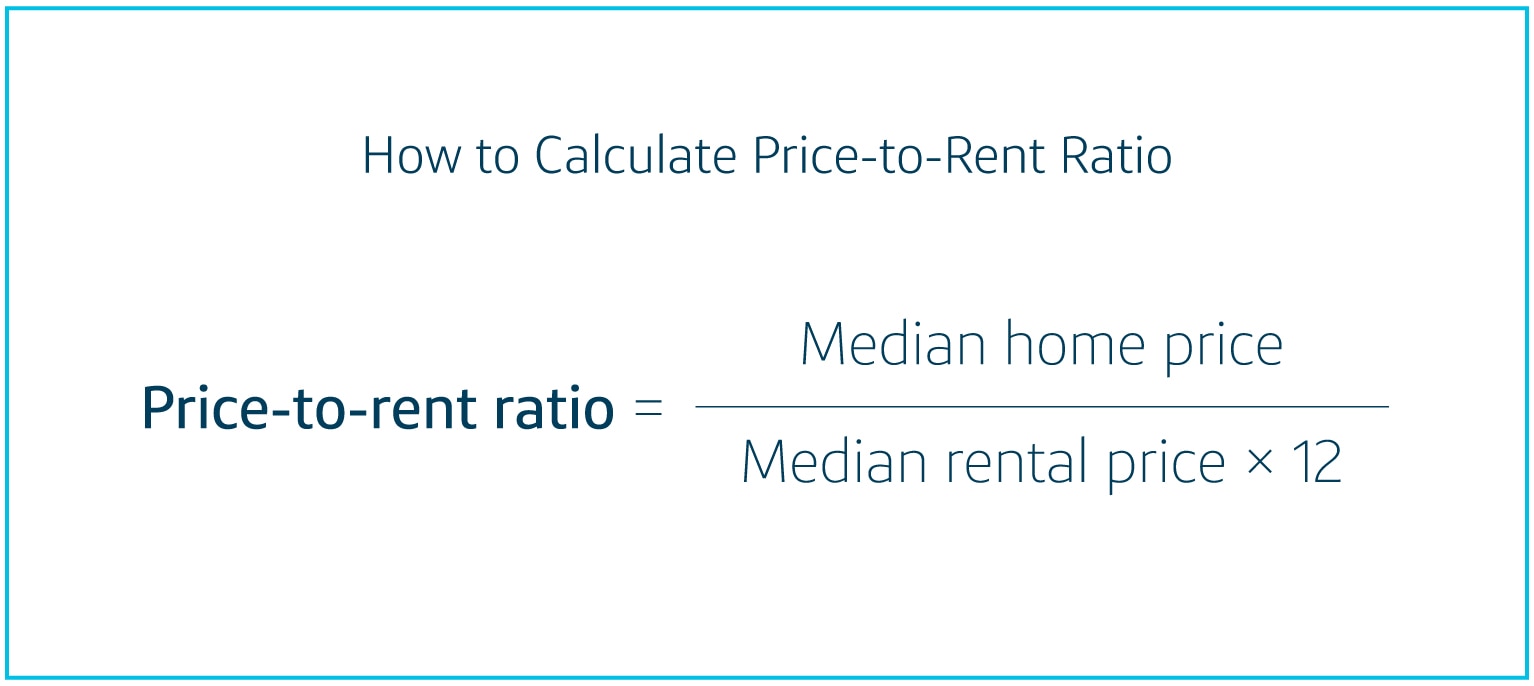

Rent vs. buy calculator

Still deciding whether you should rent or buy? It may be helpful to run some numbers. A price-to-rent ratio can help you compare current home prices to annual rents in an area.

A ratio of 16 or more can signify that renting could be the better option, while a ratio of 15 or less could mean that buying a home may be financially beneficial.

You’ll need to find an area’s median home price and median yearly rent to get started. Once you have these numbers, you can plug them into the formula below.

Renting vs. buying in a nutshell

Deciding whether to buy or rent a home isn’t always easy. It’s a personal choice that may depend on several factors, like current real estate market conditions, your lifestyle and more.

When it comes to renting versus buying, both choices have potential pros and cons. It’s important to do your research and understand how your overall financial situation—including your credit scores—could affect your options.

You can read more about the role credit scores play in renting or buying a home. If you’re curious about your scores, you can monitor your credit for free with CreditWise from Capital One.