Credit score ranges: What they are and what they mean

Anytime you apply to borrow money—whether you’re using it to buy a home, lease a car or get a credit card—lenders might consider your credit scores, which typically range from 300 to 850.

You might have been told your credit scores need to be within a certain range to qualify for certain loans. But what are the credit score ranges? And how do they work?

What you’ll learn:

-

A credit score is a three-digit number lenders use to make decisions about things like applications, credit limits and interest rates.

-

FICO® and VantageScore® are two credit-scoring companies. They calculate credit scores based on information in credit reports.

-

FICO’s and Vantagscore’s most popular credit scores range from 300 to 850.

What are the credit score ranges?

Credit scores are three-digit numbers that give an indication of creditworthiness. Companies such as FICO and VantageScore calculate credit scores using complex formulas called scoring models. These models use information in credit reports to determine the scores.

Both FICO and VantageScore produce credit scores that range from 300 to 850, and each company breaks down that range into a number of smaller categories. Here’s a closer look at FICO’s and VantageScore’s credit score ranges:

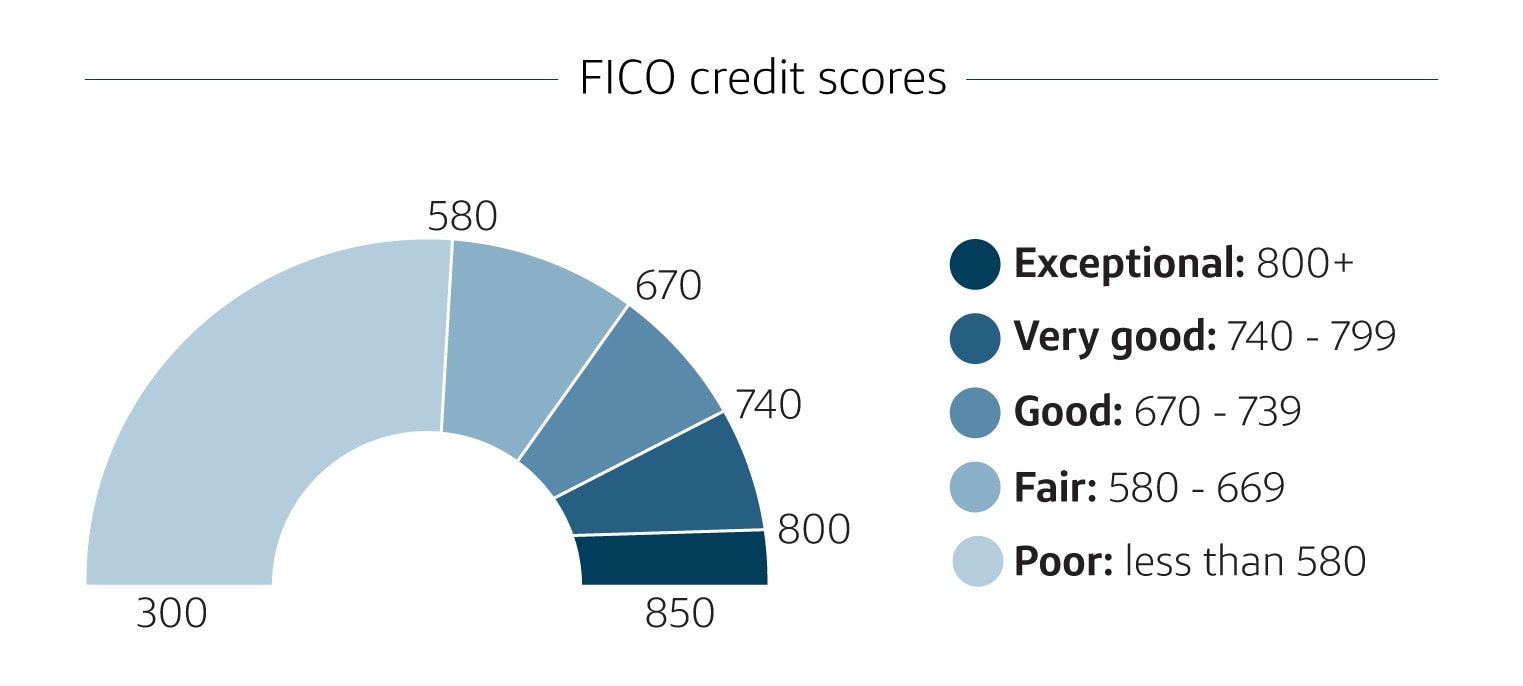

FICO credit score ranges

FICO scores are calculated using a combination of data like payment history, total amounts owed, new credit and length of credit history. Here are the ranges according to FICO:

-

Poor: Less than 580

-

Fair: 580-669

-

Good: 670-739

-

Very good: 740-799

- Exceptional: 800-850

Source: MyFICO.com

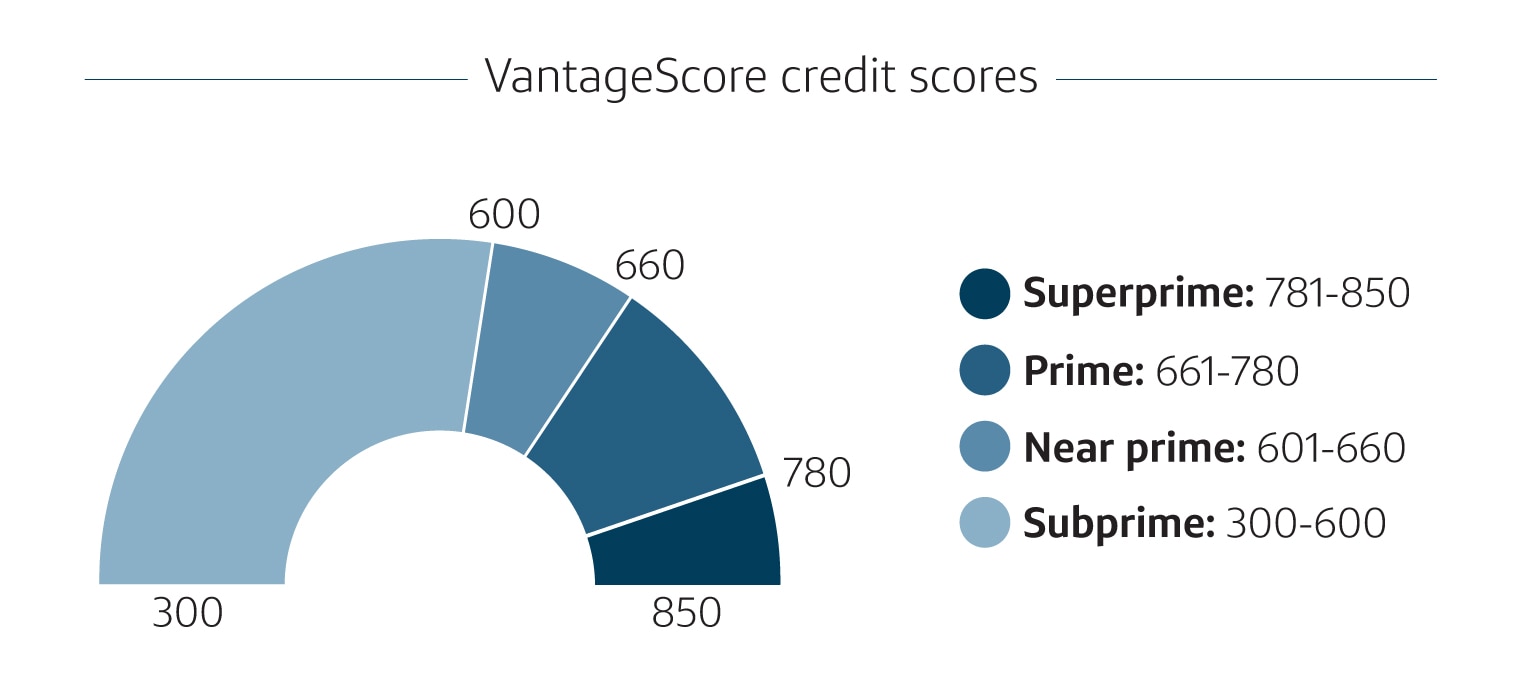

VantageScore credit score ranges

VantageScore, whose scoring models include VantageScore 3.0 and VantageScore 4.0, calculate scores by using data similar to FICO. But VantageScore weighs them differently. Here are the credit score ranges according to VantageScore:

-

Subprime: 300-600

-

Near prime: 601-660

-

Prime: 661-780

- Superprime: 781-850

Source: VantageScore.com

What do credit score ranges mean?

Credit score ranges give lenders an idea of how likely a potential borrower is to repay their debts. And knowing which category you fall into can give you an idea of the types of credit cards and interest rates you might qualify for.

Here’s a general overview of score ranges and what they mean:

What is a bad credit score range?

According to FICO, a poor credit score falls below 580. For VantageScore, its subprime category includes scores between 300 and 600.

If you have bad credit scores, qualifying for new credit or getting a mortgage for a house might be more difficult. If you can qualify, you might not be able to get the most-favorable loan terms.

What is a fair credit score range?

FICO and VantageScore differ slightly on what counts as a fair credit score: FICO says fair scores fall between 580 and 669. VantageScore says fair, or near-prime, scores are between 601 and 660.

Having fair credit generally puts you near the middle of credit score ranges. It may give you more credit opportunities than poor credit, but improving your scores could help you get better terms.

What is a good credit score range?

FICO breaks down the good credit range into good (670-739) and very good (740-799). VantageScore says its good, or prime, credit range is between 661 and 780.

Having a good credit score can help you qualify for more financial products like home and auto loans and credit cards with better interest rates.

What is an excellent credit score range?

FICO calls its highest score range exceptional, and that applies to any score between 800 and 850. VantageScore rates any score from 781 to 850 as superprime.

Excellent credit scores can help you get the best rates and terms on premium credit cards and loans, mortgages, and other lines of credit.

Factors that affect your credit scores

Credit-scoring models use a handful of similar factors to determine credit scores. But the importance or weight of each factor varies by model. Here are factors the Consumer Financial Protection Bureau says may affect your credit scores:

-

Payment history: Payment history can show how reliable a borrower is when it comes to repaying debt.

-

Total amounts owed: This considers the amount of unpaid debt you have across all your accounts and includes your credit utilization ratio.

-

Credit age: If you’ve had credit accounts open for a long time, it can indicate that you’re a lower risk to creditors.

-

Credit mix: This takes into account revolving credit, like credit cards and lines of credit, and installment loans, like car loans and mortgages. Having a combination can show you have experience handling multiple loans.

- New credit applications: When you apply for new credit, it triggers a hard credit inquiry. This can have a small negative effect on your credit scores. If you open a lot of credit accounts in a short time, it can give lenders a negative impression.

Factors that don’t affect your credit scores

These are some of the factors that don’t affect your credit scores:

-

Race

-

Religion

-

Sex

-

Marital status

-

Where you live

-

Where you were born

-

Whether you check your own credit reports and scores

-

Child or family support obligations

How to check your credit scores

There are a few places you can go to check your credit scores, including:

-

Your credit card issuer

-

Credit bureaus like Experian®, Equifax® and TransUnion®

-

Credit-scoring companies

-

Credit counselors

CreditWise from Capital One also lets you check your credit score for free anytime—without hurting your credit. It’s available for everyone, even if you’re not a Capital One cardholder. You can also get free copies of your credit reports at AnnualCreditReport.com.

Key takeaways: Credit score ranges

Your credit score range can give you an idea of your credit health. But you don’t necessarily need to achieve any particular milestone before being approved for a credit card. For example, Capital One has credit cards for people with fair credit scores. And when used responsibly by doing things like making payments on time each month, you can use a credit card to build credit.

Compare cards and explore digital features from Capital One

If you’re new to credit or searching for your next credit card, Capital One can help:

-

See whether you’re pre-approved for credit cards without harming your credit scores.

-

If you’re looking to build your credit with responsible use, explore cards for people with fair credit.

-

Earn unlimited 1.5% cash back on every purchase, every day with a cash back rewards card.

- Monitor your credit report and score with CreditWise from Capital One. It’s free for everyone, and using it won’t hurt your credit.