How to build wealth: 10 tips that can help

What qualifies as wealthy? The word means different things to different people. But a 2022 survey by investment company Charles Schwab found it takes a net worth of $2.2 million to be considered wealthy and a $774,000 net-worth threshold to be financially comfortable.

If you’re wondering how to build your wealth—whether it’s so you can buy a home, pay for your children’s college education or retire comfortably—here’s a look at some tips that could help.

Key takeaways

- When building wealth, it can help to get a handle on how much money you’re saving and spending.

- To build wealth, it helps to have a positive net worth.

- Setting realistic financial goals and investing in products like stocks, bonds and mutual funds are two ways you might be able to propel your wealth-building plan.

What is wealth building?

Your definition of wealth probably depends on your own experiences. As the Federal Reserve Bank of Dallas puts it, “Some people consider themselves wealthy because they live in a very expensive house and travel around the world. Others believe they are wealthy simply because they’re able to pay their bills on time.”

Generally, though, wealth refers to the combined value of your assets subtracted by the total amount of your debt. The assets may include a bank account, investments, a retirement account, a house or a car. The debts may include your mortgage, credit card bills and student loans.

However you define wealth, the process of becoming wealthy is known as wealth building. At its core, wealth building encompasses:

- Setting a budget.

- Saving and investing money.

- Curbing debt.

Here’s a look at some steps that you might take as part of a wealth-building strategy.

1. Understand net worth

Net worth represents the value of your assets after excluding your debts. Knowing your net worth can help you determine your next steps toward building wealth.

You can calculate your net worth by subtracting the dollar amount of your debts from the dollar value of your assets. If the total asset value exceeds the total debts, you have a positive net worth. But if the total debts exceed the total asset value, you have a negative net worth.

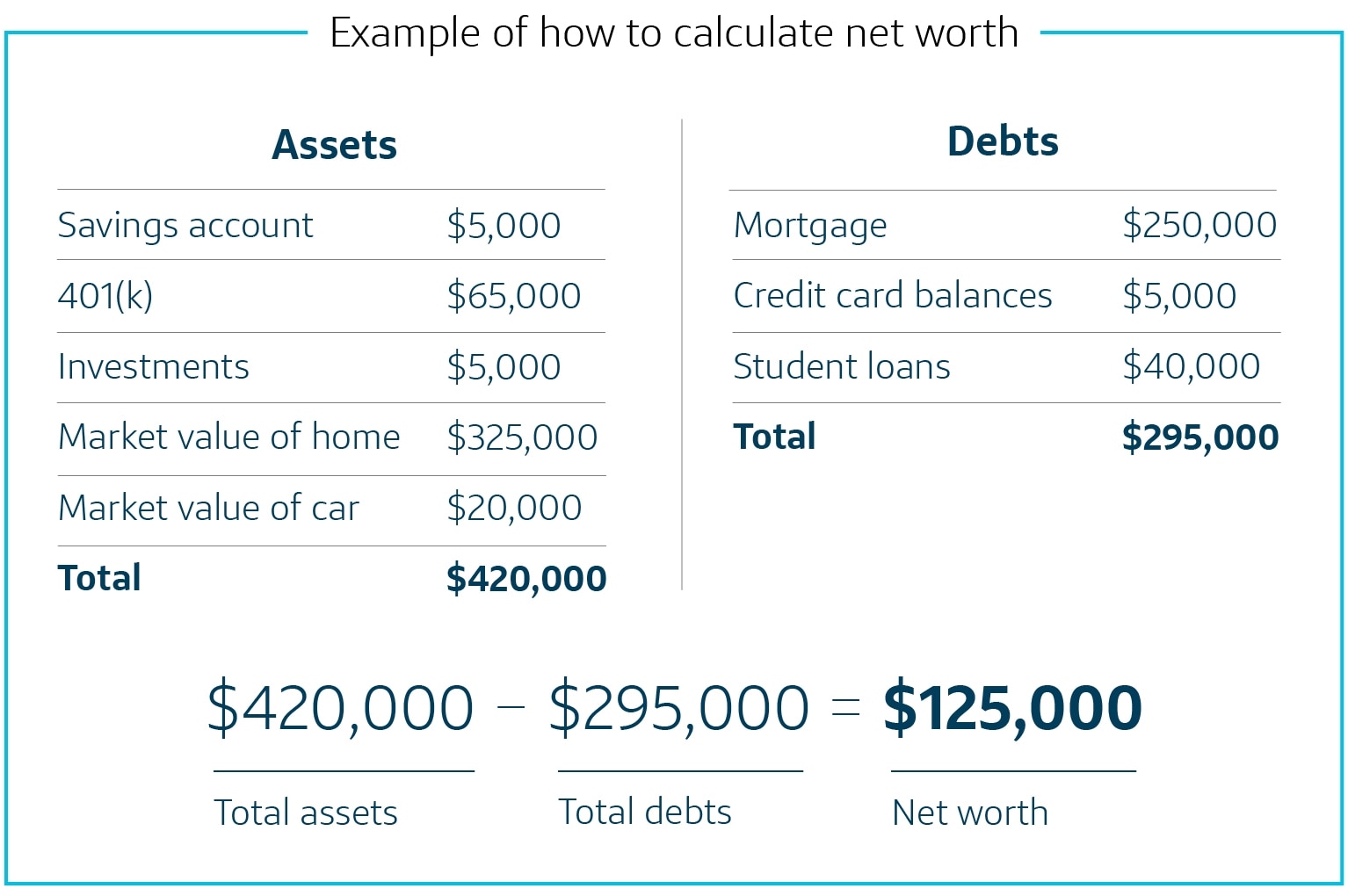

Here’s a chart showing how to calculate net worth using the assets and debts of Jessica, a fictional 30-year-old.

Doing the math, it turns out Jessica has a positive net worth of $125,000 ($420,000 - $295,000 = $125,000). Good news for Jessica: That’s higher than the average. According to the Federal Reserve’s 2019 Survey of Consumer Finances, the average net worth of an American adult under 35 is $76,340.

2. Set financial goals

Financial goals can be short-term, mid-term or long-term. A short-term financial goal might be saving money for a vacation. A mid-term financial goal might be wiping out your student loan debt, and a long-term financial goal might be investing money for retirement.

Setting financial goals—and then achieving them—can help put you on the path toward financial security.

So how do you set these goals? Here are some steps that might help:

- Determine what matters most to you. For example, are you eager to eliminate your student loan debt, or are you laser-focused on retiring comfortably?

- Come up with a list of short-term, mid-term and long-term financial goals. Make sure your goals are realistic to avoid getting unnecessarily discouraged.

- Assess your income and expenses. Review the money coming in and going out every month, and then create a monthly budget to keep your financial plan on track.

- Monitor your success. Keep track of the goals you’ve met and those you still aim to reach. As part of this step, consider dividing each long-term goal into bite-size, short-term targets to make them easier to achieve.

- Make adjustments as needed. Accept that your goals might have to change over time. For example, a job layoff or an unexpected hospital stay might change your situation and require you to rethink your goals.

3. Earn income

Income is a cornerstone of building wealth. There are three types of income you can rack up:

- Active income: Active income, also called earned income, refers to income you make from the work that you do. This could be from a full-time job or from a part-time side gig like driving for a rideshare service or tutoring high school students.

- Passive income: Passive income, or unearned income, comes from things like short-term rental properties and benefits like child support, Social Security and unemployment.

- Portfolio income: Portfolio income includes things like interest earned on a savings account, dividends distributed by companies you own stock in and capital gains from selling shares in a mutual fund.

4. Save money automatically

Automating your savings can be a simple way to build wealth. You could consider setting up regular transfers from a checking account to a high-yield savings account or diverting some of each paycheck to a savings account.

How much money should you allocate to savings? One approach that people use is the 50-30-20 rule. This way, you put 50% of your monthly income toward basic needs like housing and food, 30% toward “wants” like travel and entertainment and 20% toward savings, including an emergency fund and a retirement account.

5. Spend money consciously

How does conscious spending work? You concentrate on spending wisely while not depriving yourself of all of your fun, nonessential spending. For instance, you might:

- Create a shopping list. Sticking to what’s on your list when you’re at, say, the grocery store can prevent you from spending money on items you might want but don’t need.

- Compare prices before making a purchase. By doing some research, you stand a better chance of finding the best deal.

- Set a limit on how much you’ll spend on a big purchase. Having a maximum spend in mind if you’re shopping for a new TV, for example, could help you stay within a range that’s reasonable for you.

- Consider delaying purchases. Waiting a day or two before swiping your debit or credit card might help you think more rationally about whether you really need a particular item.

Setting up and sticking to a budget can help you spend consciously. Tracking your monthly personal finances can be done with a spreadsheet, an app or an old-fashioned pen and paper.

6. Pay off high-interest debt

If you’re able to, paying off high-interest debt can free up money to build wealth through savings or investments and other means. It can also boost your credit scores and decrease the amount of interest you’re paying.

How do you tackle your high-interest debt? Some methods are:

- Debt avalanche: The debt avalanche method involves eliminating your highest-interest debt first, then moving to the debt with the next-highest interest rate and so on. It’s still important to make the minimum payment on all your debts though. These debts may include credit cards, car loans, student loans, personal loans and medical bills.

- Debt snowball: Instead of focusing on the debt with the highest interest rate, the debt snowball method involves paying off the debt with the lowest balance first, followed by the next-lowest balance and so on. Similar to the avalanche method, it’s important not to ignore other debts completely. This method can lead to quick victories that can stimulate your debt-reduction efforts.

- Debt consolidation loan: Consolidating some of your debts—a personal loan and a credit card, for example—into one loan payment can simplify the debt-payoff process. This can be an attractive option if the interest rate on a debt consolidation loan is lower than the interest rates for the debts being consolidated.

- Balance transfer: A balance transfer enables you to shift a balance from a higher-interest credit card to a credit card with a low or even 0% annual percentage rate. Keep in mind that there may be a balance transfer fee and that the new card’s rate may only be for an introductory period.

- Credit counseling: A nonprofit credit counselor may be able to negotiate directly with lenders on your behalf to extend repayment periods, lower interest rates and waive fees.

7. Build an emergency fund

An emergency fund can help you cope with an unplanned expense or circumstance, like a huge car repair bill or a job layoff. Financial experts generally recommend that your emergency fund contains enough money to cover at least three months’ worth of household expenses.

One way to build an emergency fund is to automatically deposit money into a special account regularly, like every week or every month. It can be motivating and satisfying to watch even small amounts add up.

8. Invest your savings

Investment does come with risk. And there are different levels of risks and returns, depending on the investment. But being an investor could help your money grow so that you can reach long-term financial goals. Vehicles for investing include:

9. Work with a financial professional

Financial professionals like certified financial planners, financial coaches, investment advisers or wealth managers can provide financial advice to help you manage your money and achieve your financial goals. For example, they might help you with budgeting or recommend investment strategies.

When choosing who to work with, it’s a good idea to comparison shop to weigh the services on offer and the fees and costs involved. You can also use Investor.gov’s search tool to make sure your financial professional is licensed and registered.

10. Protect the wealth you build

Once you’ve built some wealth, it’s a good idea to protect it. A common way to do that is through insurance. This could include:

- Property insurance for your car or home.

- Health insurance for you and your family.

- Disability insurance in case you become ill or injured and can’t work.

- Life insurance for loved ones after you die.

- Long-term care insurance in case you need to live in a nursing home or assisted living facility.

Other ways to preserve your wealth include diversifying your investments to reduce risk, keeping a close eye on your spending and seeking ways to ease your tax burden.

How to build wealth in a nutshell

Building wealth takes time and effort. But a combination of sensible saving and spending practices can put you in a better position to reach your financial goals.

To aid your wealth-building journey, learn about the seven habits to help you achieve financial freedom.