Is 600 a good credit score?

Whether 600 is considered a good credit score depends on a lot of factors, including who is judging it and why. There’s no definitive answer. Because what’s good for one loan or lender may not be the same for another. Plus, most people have multiple credit scores.

But with information from authorities like the Consumer Financial Protection Bureau (CFPB) and credit-scoring companies, you can learn what a 600 credit score might mean for you. Plus, what you can do to raise your scores.

What you’ll learn:

- Some credit-scoring companies say 600 credit scores are considered fair or poor, but there isn’t a single answer to whether 600 is a good credit score.

- Credit scores depend on many factors, including who calculates it, when it’s calculated and what credit report information is used as part of the calculation.

- Student credit cards, credit cards for fair or building credit, and secured credit cards are designed for people who are working on their credit.

- You can improve your credit scores by using a credit card responsibly. That means doing things like paying statements on time every month.

- You can use digital tools like CreditWise from Capital One to monitor your progress.

What is a 600 credit score?

First, it’s important to understand how credit scores work. Credit-scoring companies like FICO and VantageScore use information from your credit reports to calculate your credit scores using complex formulas called credit-scoring models. And because each credit-scoring model is different, your credit scores may differ depending on which credit-scoring company calculated them and what data they used.

Scores can also change depending on the type of loan the score is going to be used for and even the day the score was calculated, according to the CFPB.

Each credit-scoring company also defines its own credit score ranges. So what scores qualify as a poor, fair, good or excellent score vary.

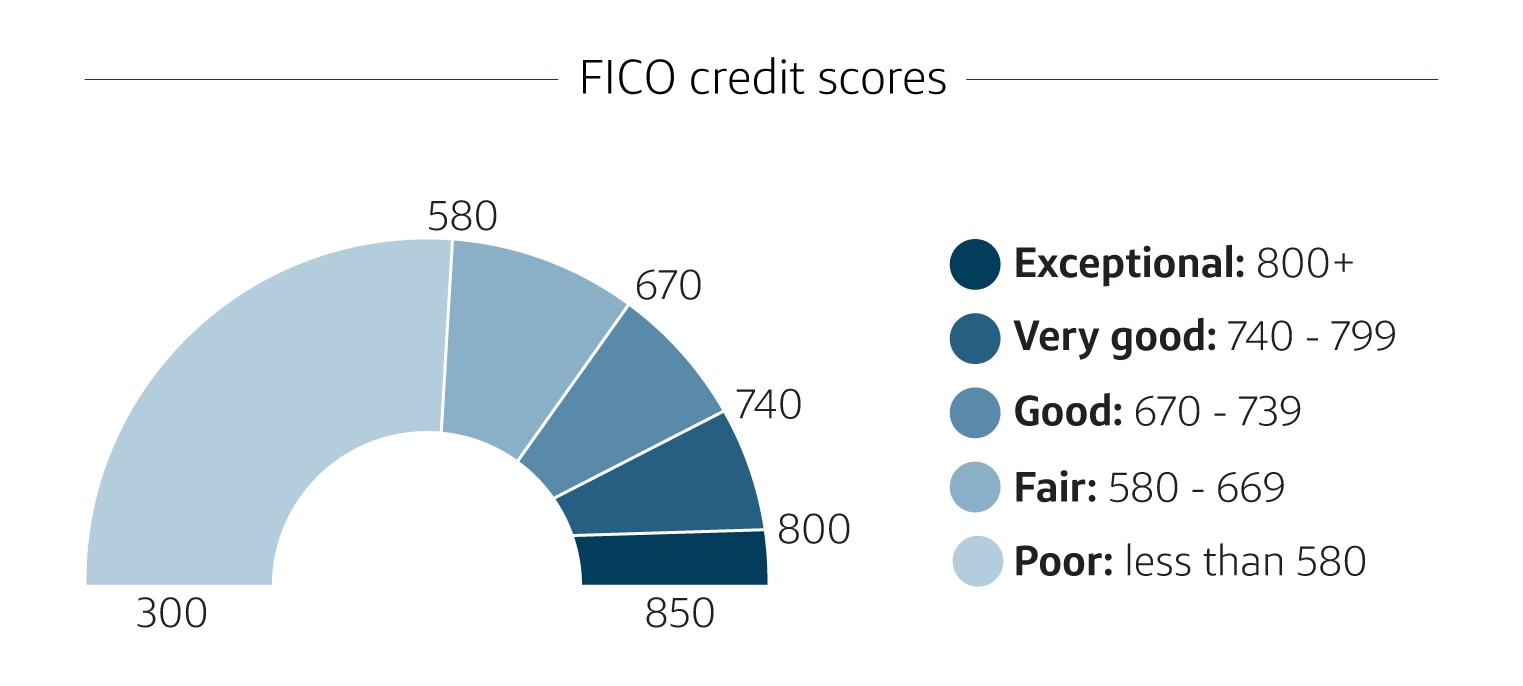

When it comes to FICO credit scores, the company says a score of 600 is considered a fair credit score. According to a report from Experian®, the average FICO credit score in America was 714 in 2022. So 600 falls below that national average.

Source: MyFICO.com

On the VantageScore range, the company says 600 scores are considered poor. But the company says fair credit scores start at 601.

Source: VantageScore.com

How are credit scores calculated?

Credit-scoring companies take information from your credit reports and enter it into complex formulas called credit-scoring models to calculate your credit scores.

Each credit-scoring model is different. And different credit-scoring companies may use data from different credit reports to calculate your scores. But there are a few common factors that can affect your credit scores:

- Payment history: Both FICO and VantageScore put significant weight on payment history when calculating credit scores. So it’s important to avoid late payments.

- Credit utilization ratio: Scoring models take your credit utilization ratio—how much of your available credit you’re using—into consideration. The CFPB recommends keeping your credit utilization ratio below 30%.

- Credit age: According to the CFPB, a long credit history can help your scores. Having a higher credit age may show that you can manage credit responsibly over a longer period of time. And that may help lenders see you as more creditworthy. So before closing a credit account, you may want to be aware of any impacts it may have on your credit.

- Credit mix: Your credit mix is important because it shows the experience you have handling different types of credit. Credit mix includes revolving credit accounts (like credit cards and personal lines of credit) and installment loans (like car loans and mortgages).

- New credit applications: When you apply for new credit, it typically triggers a hard credit inquiry, which can affect your credit scores. One hard inquiry will generally only have a minor effect. But a lot of hard inquiries may have a larger impact. The CFPB recommends only applying for the credit you need.

Remember, each credit-scoring company and credit-scoring model may weigh these factors differently. Plus, they might use data from different credit reports. So it’s normal for your FICO scores to be slightly different from your VantageScore scores.

How to check your credit score

Monitoring your credit is a great way to track your progress and make sure your credit reports are error free. With CreditWise from Capital One, you can access your credit report and credit score online without hurting your scores. It’s free for everyone, not just Capital One cardholders.

You can also request free copies of your credit reports from each of the three major credit bureaus by visiting AnnualCreditReport.com.

How to go from a fair to a good credit score

There can be a lot of benefits of having a higher credit score. Here are some things you can do to start working on improving your credit scores:

- Consistently make on-time payments.

- Keep your credit utilization ratio low.

- Check your credit reports for errors.

- Only apply for credit you need.

It’s important to note that improving your credit scores takes time. And the CFPB warns that if you see a person or company promising to fix your credit quickly, it may be a scam. If you need help with your finances, consider talking to a qualified credit counselor.

Credit cards for 600 credit score

Some credit cards are designed for people who are still building their credit. Here are a few kinds of credit cards that people with a credit score of 600 or below may want to consider:

- Student credit cards are intended for college students and recent grads who have no credit history or are still working on their credit. Some student cards even offer cash back rewards and other perks.

- If you’re not a student or recent grad, there are still credit cards for fair and building credit that may be right for you.

- Secured credit cards are another option for people with less-than-perfect credit. Secured cards require collateral to open an account. It’s typically refundable and may be the same amount as the card’s credit limit. With responsible use over time, you may be able to graduate to an unsecured card and get your deposit back as a statement credit.

No matter what kind of credit card you’re looking for, it’s important to make sure you know how to use it responsibly.

What else can you get with a 600 credit score?

Having a higher credit score may help increase your chances of getting approved for many different types of credit. But what if you’re still working on your credit but need to apply for a loan? Here are some things to know about getting different types of loans with a credit score of 600.

Can I get a personal loan with a 600 credit score?

It may be possible to get a personal loan with fair credit or poor credit. But qualifications for personal loans vary by lender. And having a lower credit score may also mean less favorable loan terms, like a higher interest rate. Or you may need a co-signer to get approved.

Can I get a car loan with a 600 credit score?

There isn’t one universal minimum credit score required to get a car loan. But like most loans, having a higher credit score may help you get approved for a loan with better terms.

Can I get a mortgage with a 600 credit score?

What credit score you need to buy a house depends on many factors, including the type of mortgage you apply for.

Generally, buyers need a credit score of at least 620 to get a conventional loan. And like with other types of loans, a higher credit score may help secure a lower interest rate.

With mortgages backed by the Federal Housing Administration, buyers need a credit score of at least 500 to qualify. But if your score is below 580, you may be required to make at least a 10% down payment. If your score is above 580, you may qualify with a down payment as low as 3.5%.

There’s no minimum credit score required for a mortgage backed by the Department of Veterans Affairs. And for USDA-backed loans, you’ll need a credit score of at least 640.

Key takeaways: Is 600 a good credit score?

A credit score of 600 might be considered either fair or poor, depending on the type of credit score and the lender reviewing it. By using credit responsibly over time, you can improve your credit scores. And having a higher credit score can open more doors for you when it comes to things like loans and credit cards.

In the meantime, you may want to look into credit cards for fair credit. And if you find a card you like, you can see if you’re pre-approved for a card offer before applying. It’s quick and won’t hurt your credit scores.