Simple interest vs. compound interest

Simple interest and compound interest are key financial concepts when it comes to borrowing, saving and investing money. Simply put, simple interest and compound interest are two different ways of calculating the interest owed on a loan or the interest earned on savings or investments.

As it relates to loans, simple interest refers to the amount of interest paid on the principal, or original amount borrowed. In other words, the borrower does not pay interest on the interest being charged. Meanwhile, compound interest refers to the interest charged on both the principal and the accrued interest of a loan.

Simple interest and compound interest for savings and investments work in a similar way. An account holder earns simple interest only on the principal, or the initial amount of money deposited. By contrast, an account holder earns compound interest on the principal along with the accrued interest.

Key takeaways

- Most mortgages, student loans and auto loans charge simple interest.

- Simple interest typically results in lower total interest charged on a loan.

- Savings accounts typically compound the interest that someone earns.

- Compound interest generally leads to more total interest accumulated in a savings account.

What is simple interest?

Simple interest means there is no “interest on interest.” With a loan, a borrower would not pay interest on accrued interest. With savings or investments, an account holder would not earn interest on accrued interest.

Among the lending products that typically charge simple interest are car loans, student loans, personal loans and mortgages.

Simple interest is less common than compound interest for savings and investment accounts.

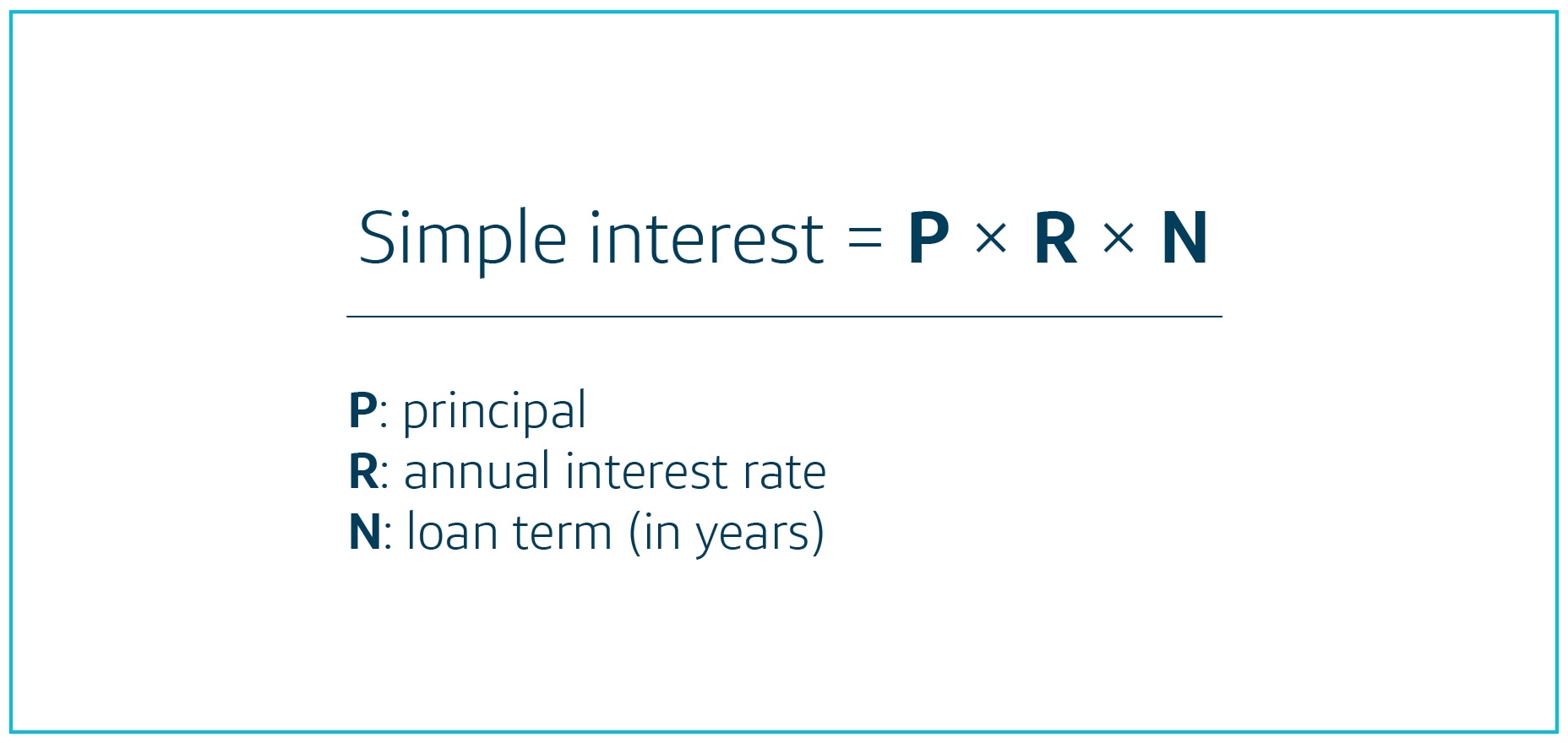

Simple interest formula

Here is how the simple interest formula works for a loan:

Here is an example of a simple interest formula for a car loan:

$40,000 (principal) x 0.06 (6% annual interest rate) x 6 (years of the loan term) = $14,400

What is compound interest?

For a loan, compound interest is the amount of money paid on the original principal, or total loan amount, plus the accumulated interest. In terms of savings and investments, compound interest is the amount of money earned on what has been saved or invested, known as the principal, plus the accumulated interest.

Lending products that may use compound interest include credit cards, student loans and personal loans. Among the savings and investment accounts that typically pay compound interest are savings accounts, CDs, bonds and money market accounts.

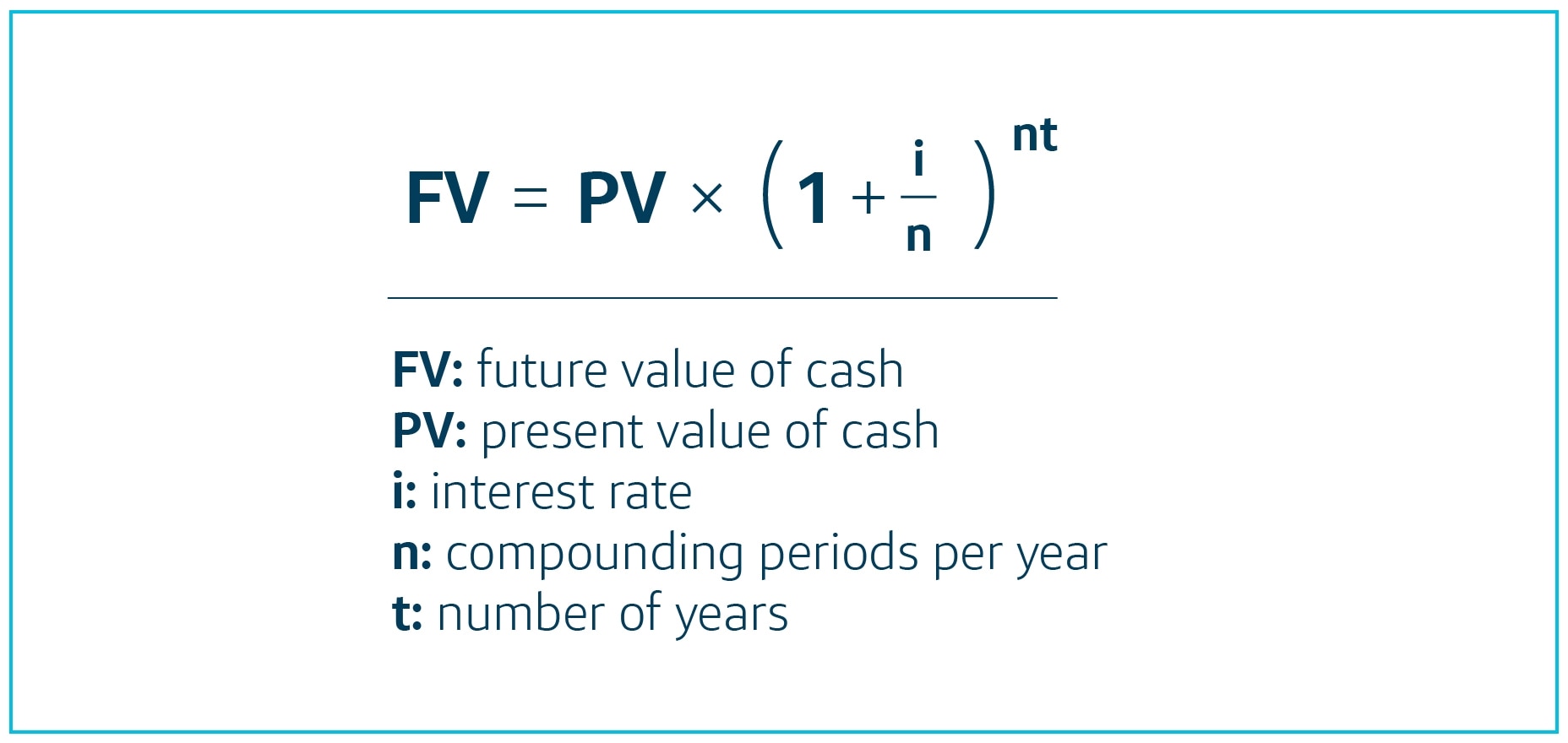

Compound interest formula

Here’s what the formula for calculating compound interest looks like for a savings account:

Here’s an example of a compound interest formula for a savings account:

A = 10,000 (1 + 0.03/365)^(365 x 10)

In this example, the principal is $10,000, the annual percentage yield (APY) is 3%, the compounding period is annual—365 days—and the number of years is 10. The result: Without adding any money to the original $10,000, an account holder would wind up with $13,498.42 after 10 years.

Compounding periods

Compounding periods for savings include annual, semiannual, quarterly, monthly and daily.

The more frequent the compounding, the more money an account holder should have in savings, if all other factors are equal. This is because compounding speeds up your savings. In other words, daily compounding should yield more money than monthly compounding, for example.

Keep in mind that although interest might be compounded daily, for instance, the compounded interest might be paid out once a month.

The chart below demonstrates how different compounding methods might affect a savings account with an initial $10,000 deposit and a 3% APY over a 10-year period:

| Initial deposit | APY | Number of years | Compounding method | Total balance |

|---|---|---|---|---|

| $10,000 | 3% | 10 | Quarterly | $13,483.49 |

| $10,000 | 3% | 10 | Monthly | $13,493.54 |

| $10,000 | 3% | 10 | Daily | $13,498.42 |

Of course, more frequent compounding would create an even bigger impact if an account holder made regular deposits that added to the original balance. Using the same figures from the previous chart, the following chart shows how a $250-a-month deposit would affect the total balance over time:

| Initial deposit | Monthly deposit | APY | Number of years | Compounding method | Total balance |

|---|---|---|---|---|---|

| $10,000 | $250 | 3% | 10 | Quarterly | $48,318.35 |

| $10,000 | $250 | 3% | 10 | Monthly | $48,428.89 |

| $10,000 | $250 | 3% | 10 | Daily | $48,482.64 |

Time value

Under the concept of time value, an amount of money is perceived to be worth more now than it would be in the future. Why? Because money that someone holds now can:

- Be invested and earn interest

- Lose its purchasing power due to inflation

- Be more of a certainty than any money someone may or may not have in the future

Compounding demonstrates the effect of the time value of money into the future when interest is tacked onto an initial deposit.

Here’s the formula for computing the future value of money that someone might be keeping in savings:

What is the difference between simple and compound interest?

The major difference between simple and compound interest involves the advantages and disadvantages when the interest rate applies to a loan or to a savings or investment product.

Simple interest vs. compound interest: Which is better?

Whether simple interest is better than compound interest depends on whether you’re a borrower or a saver and investor.

If you’re a borrower, simple interest typically is better than compound interest. Why? Because a borrower pays interest only on the principal and not on the accumulated interest if they have a simple interest loan. On the other hand, a borrower pays interest on the principal and accumulated interest if they have a compound interest loan.

So for the same loan with the same terms, a borrower should save money on a simple interest loan vs. a compound interest loan. Keep in mind that regardless of simple interest or compound interest, a taxpayer may be able to take a tax write-off on interest paid on a loan.

Meanwhile, compound interest typically is better than simple interest for savers and investors. If a savings or investment account compounds the interest, someone earns interest on the principal as well as the accumulated interest. But if a savings or investment account offers simple interest, someone earns interest only on the principal and not the accumulated interest.

Therefore, a saver or investor should gain more money with compound interest than simple interest.

Simple interest and compound interest in a nutshell

Simple interest and compound interest are important concepts to know about when it comes to someone’s personal finances.

Simple interest might grant someone less interest on a savings or investment account but might save them money on a loan in the form of lower interest. The opposite is true for compound interest, which may mean more interest for a saver or investor but result in higher interest costs for a borrower.