What is a bad credit score?

You may know that credit scores represent creditworthiness. And that potential lenders might use your scores to make decisions about loans and credit. But what does it mean to have a bad credit score?

What’s considered a bad score depends on the lender and the loan or credit card. But credit-scoring companies offer clues. For example, FICO® says a poor score is one that falls below 580.

Keep reading to learn more about credit scores, how they might affect you and a few tips that may help improve your scores.

Key takeaways

- A bad credit score may be one that falls into credit score ranges that FICO and VantageScore® consider poor or very poor.

- A poor FICO credit score might be considered less than 580. A poor VantageScore credit score might be 600 or less, with very poor scores being 499 or less.

- It’s possible to improve a bad credit score by using credit responsibly. That means doing things like paying bills on time and reducing overall debt.

- You can see where your credit stands—without hurting it—by using a free service, such as CreditWise from Capital One.

What’s considered a bad credit score?

Credit decisions—and what’s considered a bad score—are ultimately determined by potential lenders. But you can get an idea of what’s considered bad based on looking at what credit-scoring companies have to say.

The most commonly used credit scores come from FICO and VantageScore. They range from 300 to 850, according to the Consumer Financial Protection Bureau (CFPB).

But those companies have different versions of credit scores and scoring models. That means people have more than one score out there.

One thing FICO and VantageScore do agree on is that the higher your credit score, the better: “In general, people with higher scores can get more credit at better rates,” VantageScore says. Having lower credit scores could make it difficult to get approved for credit cards, mortgages, car loans and more.

What is a bad FICO credit score?

A bad FICO credit score may fall into the poor FICO range. And FICO considers a credit score to be poor if it’s below 580.

Source: MyFICO.com.

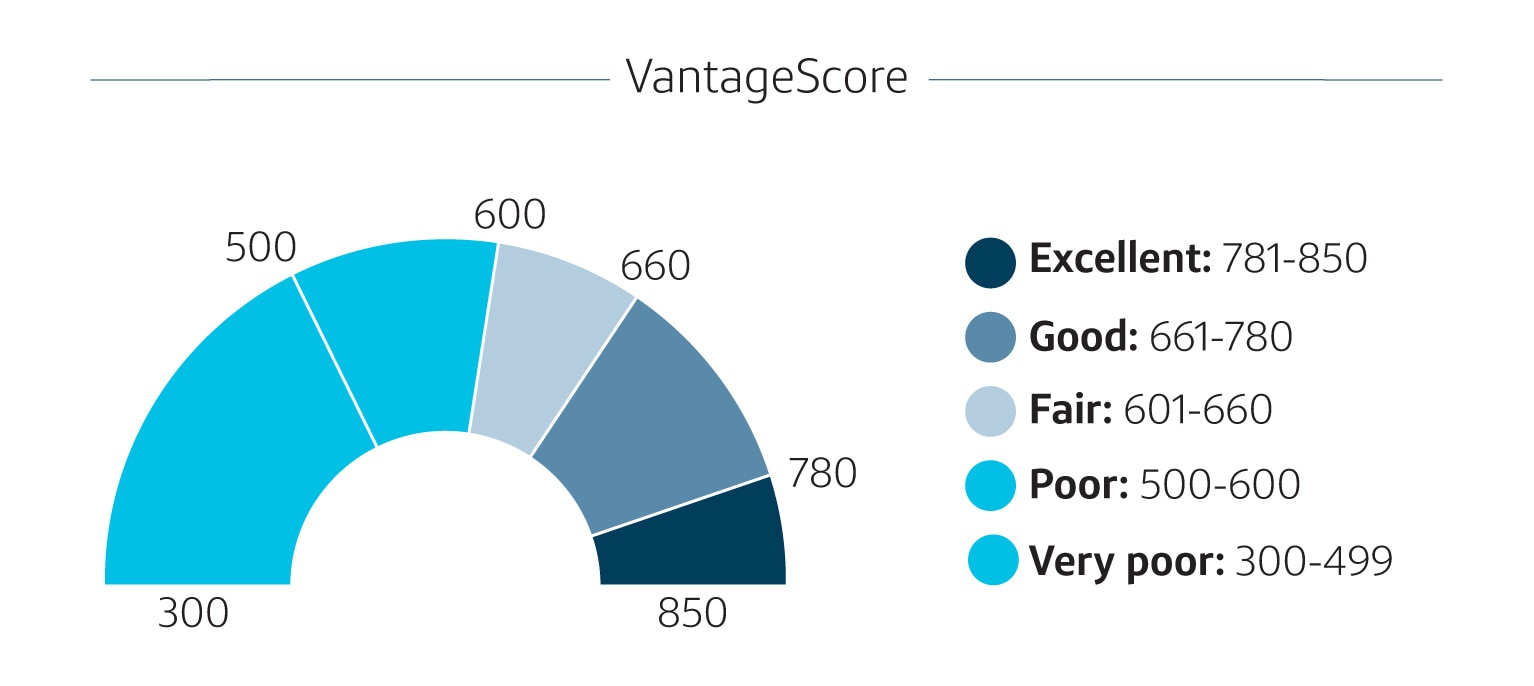

What is a bad VantageScore credit score?

A bad VantageScore credit score may fall into the poor or very poor credit score ranges. A poor VantageScore credit score falls between 500 and 600, while a very poor score falls between 300 and 499, according to Experian—one of the three nationwide credit bureaus.

Source: Experian.com.

What factors influence your credit scores?

There are a few factors that credit-scoring companies use to determine credit scores. And according to the CFPB, they’re all calculated based on data from credit reports.

Scoring models might use the following information from your credit reports:

- Payment history: How often you pay your bills on time

- Account history: How long you’ve had credit and loans open

- Debt: How much you owe across all accounts

- Credit utilization: How much credit you use compared to your total available credit

- Recent inquiries: How many times creditors have pulled your credit report and how many new loans you have

- Credit mix: How many kinds of credit you use, including credit cards and installment loans

Keep in mind that past bankruptcies, foreclosures and collections may also factor into your credit score. And the CFPB says those things can sometimes affect scores for 10 years or longer.

How bad credit can affect you

Everyone’s situation is different, but a bad credit score could affect your financial goals and lending options. Here are some instances where a higher credit score can be helpful:

- Credit cards: If you’re able to improve your credit scores, you might increase your chances of qualifying for credit cards with higher credit limits and lower rates.

- Loans and mortgages: A higher credit score could also help you get approved for auto loans, mortgages and other types of loans. And more loan options might mean you can shop around for better terms on things like interest.

- Interest rates: In many cases, a higher credit score could help you pay less in interest, which is the price you pay for borrowing money. And paying less in interest could help you save money over time.

- Rental applications: When you apply for a lease, your potential landlord could look at your credit when reviewing your rental application.

- Employment applications: Some potential employers may pull your credit reports as part of a background check. But they have to get your permission first. And if you decline or have bad credit, you might not be considered for the role.

- Insurance premiums: In some states, your credit history could influence the cost of things like car insurance. Bad credit might mean higher premiums.

- Deposits: A stronger credit score might allow you to skip security deposits to set up service with utility companies and cellphone providers.

Ways to help improve bad credit scores

It’s possible to improve your credit scores over time. Here are a few good financial habits that can help you do just that:

- Review your credit report: You can get a sense of where you stand by requesting free copies of your credit reports from AnnualCreditReport.com. You could also monitor your credit with CreditWise from Capital One without hurting your score. It’s free for everyone, not just Capital One customers.

- Pay your bills on time and catch up on overdue bills: Your payment history plays the biggest part in some FICO and VantageScore credit-scoring models. The CFPB says getting current on payments and making on-time payments from now on could help improve your credit score. If you’re unable to pay your bills, consider reaching out to your lender about what options might be available.

- Become an authorized user: The CFPB says being an authorized user could help your credit if the card’s activity is reported to credit bureaus and the card is used responsibly. But things like missed payments could have negative effects on both you and the original cardholder.

- Consider a secured credit card: With secured credit cards, you’re required to put down a security deposit before you start to spend. Some credit card companies report secured card activity to credit bureaus. If approved for a secured credit card, you could help your credit score by using the card responsibly.

- Keep some of your credit available: Your credit utilization—the percentage of your available credit that’s in use—can also affect your credit score. The CFPB recommends using 30% or less of your credit limits across all your accounts.

Bad credit in a nutshell

You’re not alone if you have a less-than-perfect credit score. But practicing responsible financial habits like paying your bills on time, repaying existing debt and not maxing out your credit cards can help you rebuild your credit.

When used responsibly, a credit card can also be a helpful tool to help you boost your scores. Capital One offers several credit cards for people trying to build credit with responsible use.