What is APR and how does it work?

APR, or annual percentage rate, represents the price of borrowing money. APR is expressed as a yearly percentage that includes the loan’s interest rate plus additional costs such as lender fees, closing costs and insurance.

Read on for a deeper dive into APR, including how it works, the different types of APR and more.

What you’ll learn:

-

APR represents the price you pay for a loan. It typically includes interest rates and any fees.

-

The APR can sometimes be the same as the interest rate. That’s the case for most credit cards.

-

APR may be fixed or variable, meaning the rate may stay the same or it might change with market factors.

- Credit card APRs may vary based on the type of transaction and how the credit is used.

Why is APR important?

Understanding how APR works can help you make more informed credit decisions. For example, if you’re deciding between credit cards, you can compare APRs to help determine which lender and card might work best for you.

APR vs. interest rate: What’s the difference?

An interest rate shows the amount of money it costs to borrow the principal loan amount. An APR is the interest rate plus any fees, closing costs or insurance. So if no such fees exist, the APR and interest rate may be the same. That’s usually the case for credit cards.

Find out more about the difference between interest rate and APR.

How does APR work?

APR represents the cost of borrowing money. It includes the yearly interest rate as well as any fees, including things like:

-

Origination fees

-

Transaction fees

-

Broker fees

-

Closing costs

With credit cards, if you pay off your balance on time every month, you won’t be charged any interest. But if you carry a balance from month to month, you’ll be charged for the unpaid portion.

Your credit history and credit scores can affect what APR you’re offered and whether you receive a fixed or variable rate.

Fixed APR vs. variable APR

The type of APR determines the amount you pay for what you borrow. Here’s how fixed and variable APRs work:

-

Fixed APR: A fixed APR generally doesn’t change over the life of the loan. But as the Consumer Financial Protection Bureau (CFPB) notes, that doesn’t mean the interest rate will never change. However, the issuer generally must notify you before the change occurs.

- Variable APR: A variable APR is tied to an index interest rate, such as the prime rate. If the prime rate increases, so does the variable APR. So while the loan may have a lower APR at first, the rate can increase over time. Most credit card accounts have a variable APR.

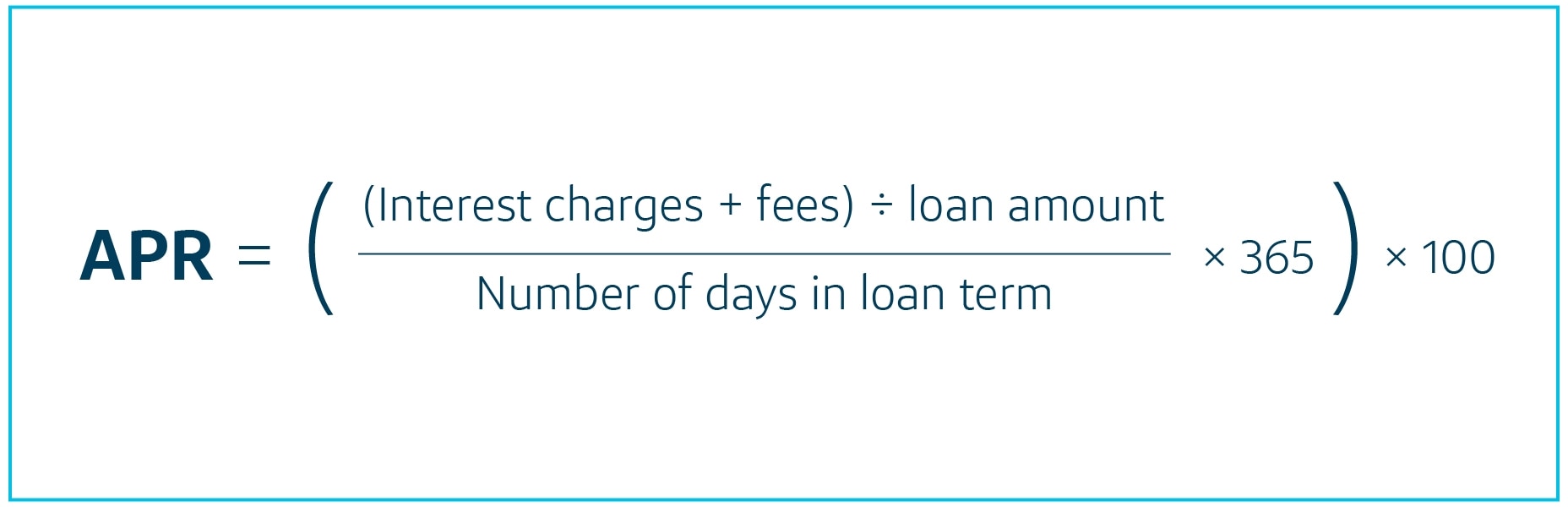

How to calculate APR

Banks and credit card issuers may use this APR formula to determine how much interest borrowers must pay on outstanding balances.

APR = (((Interest + Fees ÷ Loan amount) ÷ Number of days in loan term) x 365) x 100

APR can be calculated daily or monthly, depending on the loan or card. Credit card issuers are required to disclose how they calculate APR. In general, their calculations rely on:

-

The loan amount

-

How many days there are in the loan term for the year

-

The interest rate of the loan

- Any fees related to the loan

Types of credit card APRs

With an installment loan, your APR is either fixed or variable. But with a credit card, there are a few more APR types, depending on how you use the card.

Purchase APR

A credit card’s purchase APR is the rate that’s applied to purchases made with the card.

Cash advance APR

The cash advance APR is the cost of borrowing cash from a credit card. This rate tends to be higher than the purchase APR. Cash advances usually don’t have a grace period. This means that interest accrues immediately.

There are other transactions that might be considered cash advances, even if cash never touches your hands. These include buying casino chips, purchasing lottery tickets or exchanging dollars for foreign currency.

Penalty APR

If a borrower violates the terms of their card’s contract by doing things like missing a payment or being late with a payment, the APR on their card may increase for a period of time. That’s a penalty APR.

Be sure to check your card’s terms and any notices the issuer sends related to your account.

Promotional APRs

There are two common types of promotional APRs:

-

Introductory APR: A new credit card may come with a lower, limited-time APR. Different card issuers have different standards for what qualifies as an introductory APR, so it’s important to read the terms and conditions. For example, you may only get the introductory APR for purchases above a set amount.

- Balance transfer APR: A balance transfer may qualify a borrower for a special APR on a new or existing credit card. The promotional period may last anywhere from six to 21 months, but the balance transfer APR may only apply to the balance transferred. A separate APR can still apply for new purchases. So make sure you review all the interest rates, if there are multiple, and any fees, like a balance transfer fee or foreign transaction fees.

What’s the average APR on a credit card?

The Federal Reserve regularly reports the national average APR. As of November 2024, the Federal Reserve’s most recent available data, the national average APR was 22.8%.

5 tips to get a lower-APR card

Maintaining good credit scores can help lenders see you as a better candidate for cards with low APRs and additional benefits. Here are a few tips that can help you get and keep good credit scores:

-

Use your current card responsibly and pay your bills on time. Late payments can have a negative effect on your credit. Consider automating payments or setting reminders to help you remember.

-

Avoid getting too close to your credit limit. Generally, using a lot of your credit could be a red flag to lenders. The CFPB recommends keeping your credit utilization rate at 30% or less.

-

Keep building your credit. Credit scores are based on your experience with credit over time. That means the longer your credit report shows you paying your loans on time, the better.

-

Apply for only the credit you need. Be careful about applying for a lot of credit over a short period. It could suggest to lenders that your financial situation has changed negatively.

- Monitor your credit. Everyone has access to free credit reports from each of the major credit reporting agencies through AnnualCreditReport.com. CreditWise from Capital One is another tool that can help you monitor and track your credit. Using it won’t affect your credit, and it’s free for everyone.

Annual percentage rate FAQ

Still have questions about APR? These answers to frequently asked questions might help.

What’s the difference between APR and APY?

APY stands for annual percentage yield. It’s sometimes also known as EAR, or effective annual rate. APY is the measure of the interest you earn when you save. That’s why APY typically applies to money you place in a deposit account, not to money you borrow. APR measures the amount of interest you’ll be charged when you borrow. Read more about the differences between APR and APY.

What’s a good APR rate?

The best APR for you is one that you can manage on a card that’s suitable for you. And according to the CFPB, “the higher your credit scores, the lower your rates will be.”

How do you avoid paying APR on a credit card?

You can avoid paying interest on new purchases if you’re able to pay your credit card balance in full and on time each month. You can also avoid interest for a limited time with a credit card that has a 0% introductory APR. But once the promotional APR period ends, the card’s standard APR will apply. And if you’re carrying a balance at that point, you’ll start to see the card’s standard rate applied to the balance.

Key takeaways: What is APR?

APR is the cost of borrowing money expressed as a yearly percentage. This figure is calculated based on the loan’s interest rate and any fees that are part of its terms. The APR may be fixed or variable.

If you’re interested in a low-APR credit card, you could consider checking out credit cards from Capital One.

Explore more from Capital One

New to credit or looking for your next credit card?

-

Check for pre-approval offers with no risk to your credit score.

-

Earn unlimited 1.5% cash back on every purchase, every day, with Quicksilver.

- Explore Capital One’s credit cards for building credit with responsible use.