What is VantageScore?

If you’ve ever applied for a credit card or loan, chances are the lender checked your credit scores. And one company that calculates credit scores is VantageScore®.

VantageScore was developed by the three major credit bureaus—Experian®, Equifax® and TransUnion®. It’s one of the two major credit-scoring services lenders use, along with FICO®. Learn more about what can affect your VantageScore credit scores and the different credit score ranges.

Key takeaways

- VantageScore is a credit-scoring model that calculates credit scores, which lenders use to determine a borrower’s creditworthiness.

- VantageScore was created by the three major credit bureaus as an alternative to the popular FICO scoring models.

- VantageScore credit scores are based on a number of factors like payment history, credit utilization, credit age and recent hard inquiries.

- VantageScore considers a good credit score to fall between 661 and 780.

How does VantageScore work?

VantageScore was founded by Experian, Equifax and TransUnion in 2006. Today, it operates independently. While FICO uses credit-scoring models specific to each bureau, VantageScore created what it calls a “tri-bureau” model—using data from all three bureaus.

The first two scoring models, VantageScore 1.0 and 2.0, calculated scores ranging from 501 to 990. Since then, VantageScore 3.0 and 4.0 have begun calculating scores between 300 and 850.

VantageScore calculates credit scores based on a set of factors related to credit activity and credit history.

Payment history

Payment history tracks how reliably debt has been repaid. A late payment can stay on a credit report for up to seven years and have a negative impact on credit scores.

Credit utilization

Credit utilization measures how much available credit a person is using. You can find your credit utilization ratio by dividing the amount of credit in use by your total available revolving credit. It’s recommended to keep your credit utilization below 30%.

Depth of credit

This refers to the length of time a person has had credit accounts open. It includes oldest, youngest and average account ages. Depth of credit also covers the types of credit accounts, or credit mix. This may include installment credit, such as personal loans and mortgages, and revolving credit, such as credit cards.

Recent credit

New credit applications typically involve a hard inquiry on credit reports. Too many recent hard credit inquiries can temporarily lower credit scores and might be viewed negatively by lenders.

Balances

This factor considers the total balance of current unpaid debt. Even if payments are on time, maintaining high balances can have an impact on credit scores. And carrying a balance might negatively affect credit too.

Available credit

While this is the least influential factor in VantageScore scoring models, having more credit available can improve credit scores.

What is VantageScore 3.0?

In 2013, VantageScore introduced its 3.0 model, which provided more consistency across the credit bureaus and adopted the 300-850 scoring range. It also made it possible to rate consumers with thin credit files who may have been previously “unscoreable.” Here’s how the factors are weighted in VantageScore 3.0:

- Payment history: 40%

- Depth of credit: 21%

- Credit utilization: 20%

- Balances: 11%

- Recent credit: 5%

- Available credit: 3%

What is VantageScore 4.0?

Introduced in 2017, VantageScore 4.0 is its latest credit-scoring model. VantageScore says 4.0 has more predictive performance. And it began factoring in credit behavior patterns over time—instead of looking at a consumer’s credit in a single snapshot.

Here’s how the factors are weighted in VantageScore 4.0:

- Payment history: 41%

- Depth of credit: 20%

- Credit utilization: 20%

- Recent credit: 11%

- Balances: 6%

- Available credit: 2%

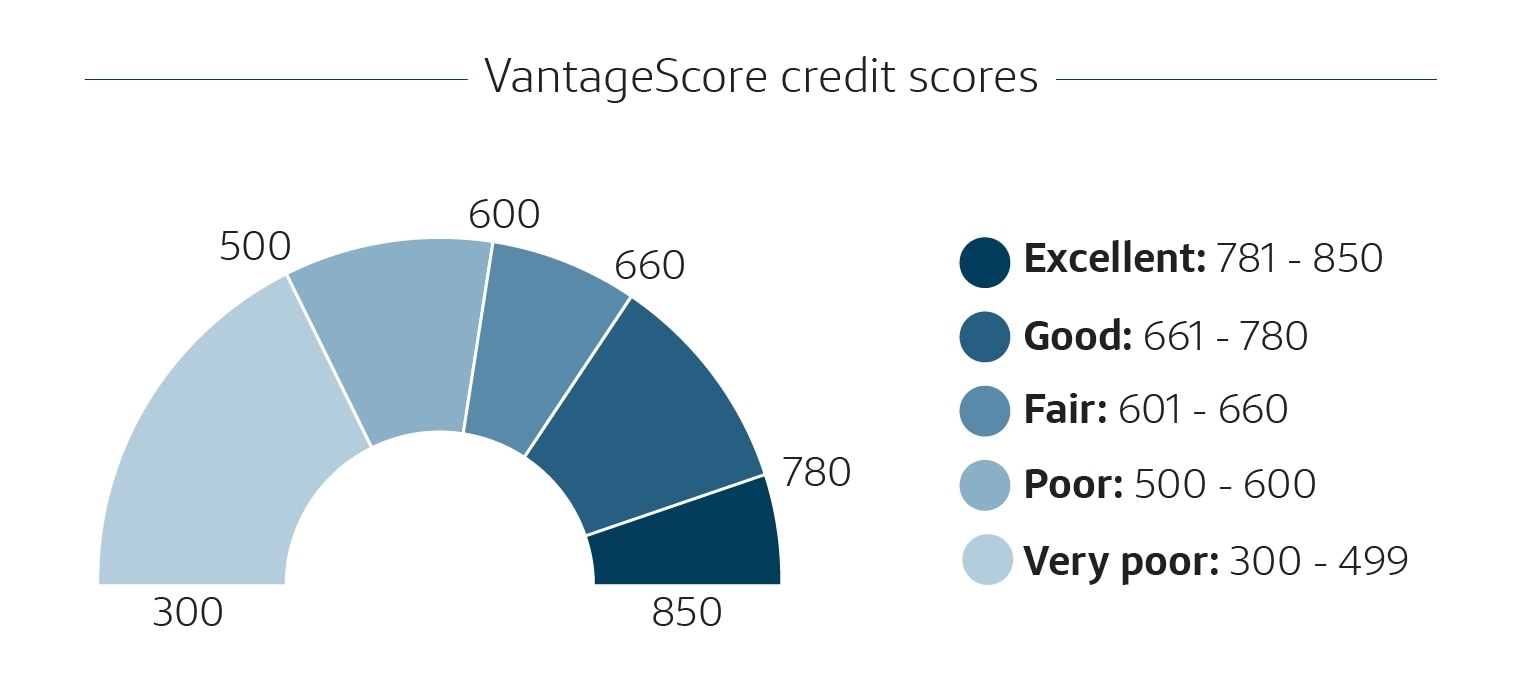

VantageScore credit score ranges

VantageScore calculates credit scores on a scale of 300 to 850. Within that scale, it says there are five credit score ranges:

- Very poor: 300-499

- Poor: 500-600

- Fair: 601-660

- Good: 661-780

- Excellent: 781-850

What is a good VantageScore?

VantageScore considers any score between 661 and 780 to be a good credit score. But lenders ultimately get to decide about a borrower’s creditworthiness. Having good credit scores might help you get approved for more credit and qualify for lower interest rates.

VantageScore vs. FICO: What’s the difference?

FICO and VantageScore are two credit-scoring companies. According to the Consumer Financial Protection Bureau (CFPB), “Most lenders still use FICO scores when deciding whether to offer you a loan or credit card, and in setting the rate and terms.” But both companies’ scores may be used by lenders to review applications for things like credit cards, student loans and auto loans.

Each company uses its own credit-scoring models to calculate credit scores. And the CFPB says that “any credit score depends on the data used to calculate it.” This means you can have several different credit scores at any given time.

FICO says it creates scores for borrowers with “at least one account opened for six months or more.” On the other hand, VantageScore scores “can often be calculated within a month of the account appearing on the credit report”—even if it was opened under six months ago.

How to see your VantageScore credit score

You can check your VantageScore 3.0 credit score with CreditWise from Capital One—it’s free, and it won’t hurt your credit. CreditWise can also alert you of any changes to your TransUnion or Experian reports.

VantageScore in a nutshell

VantageScore uses multiple scoring models to calculate credit scores. The most recent versions, VantageScore 3.0 and 4.0, offer scores on a scale of 300 to 850. And those scores might be a factor when you do things like apply for a loan or credit card.

Knowing what your credit scores are can help you understand how you might appear to lenders. Monitoring your credit with CreditWise might be a good place to start. You can also discover a few ways you might be able to improve your credit scores.