Which credit score is most accurate?

If you’re trying to figure out which credit score is most accurate, then you already know there are multiple scores out there. But one credit score isn’t necessarily more accurate than another. It’s more complicated than that.

Find out what factors make for good credit scores, how credit bureaus and credit-scoring companies fit in, and how you can monitor your credit.

What you’ll learn:

-

FICO® and VantageScore® are two popular credit-scoring companies.

-

Credit scores vary depending on the credit bureau, credit-scoring company, model used and timing of the score.

-

One credit score isn’t inherently more accurate than another. Rather than comparing scores for accuracy, it might help to compare scores at different points in time.

-

Which credit score is used can depend on the lender and what you’re applying for.

- It’s possible to check your own credit without hurting your credit scores.

What is the most accurate credit score?

There is no single credit score that’s considered the most accurate. The truth is, there are several types of credit scores and many versions of each of those scores. And while different scores are often calculated based on many of the same factors, thinking of these scores in terms of accuracy can still be misleading.

Why are my credit scores different?

The Consumer Financial Protection Bureau (CFPB) explains that it’s normal to have slightly different credit scores. That’s because scores can vary based on factors like the credit report data, the credit-scoring model and even the timing of the calculation.

Here’s a little more about what each score can depend on:

-

Which credit bureau supplied the data: Each of the three major credit bureaus—Equifax®, Experian® and TransUnion®—keeps records of credit history. But not every lender reports information to each bureau. Lenders may also report to credit bureaus at different times of the month, which can also affect calculations.

-

When the score was calculated: Credit-scoring factors change over time. This means scores vary as they change, depending on the day they were calculated. For example, as you use your card, your credit utilization goes up. When you pay your statements, it goes down.

- Which scoring model was used: Different credit reporting companies use different scoring models. And the factors affecting your credit scores can carry different weights.

Types of credit-scoring models

FICO and VantageScore use similar factors to calculate credit scores. But they weigh those factors differently.

What is a FICO score?

Originally named Fair Isaac Corporation, FICO developed the modern credit-scoring model in 1989. To this day, its scores are some of the most widely used. FICO claims its scores are used by 90% of top lenders.

The FICO credit-scoring model has been updated over the years, resulting in multiple versions of the score. FICO Score 8 is the most commonly used. But the version may vary by lender and credit product. Different FICO score versions may be used when applying for a credit card versus financing a car, for example.

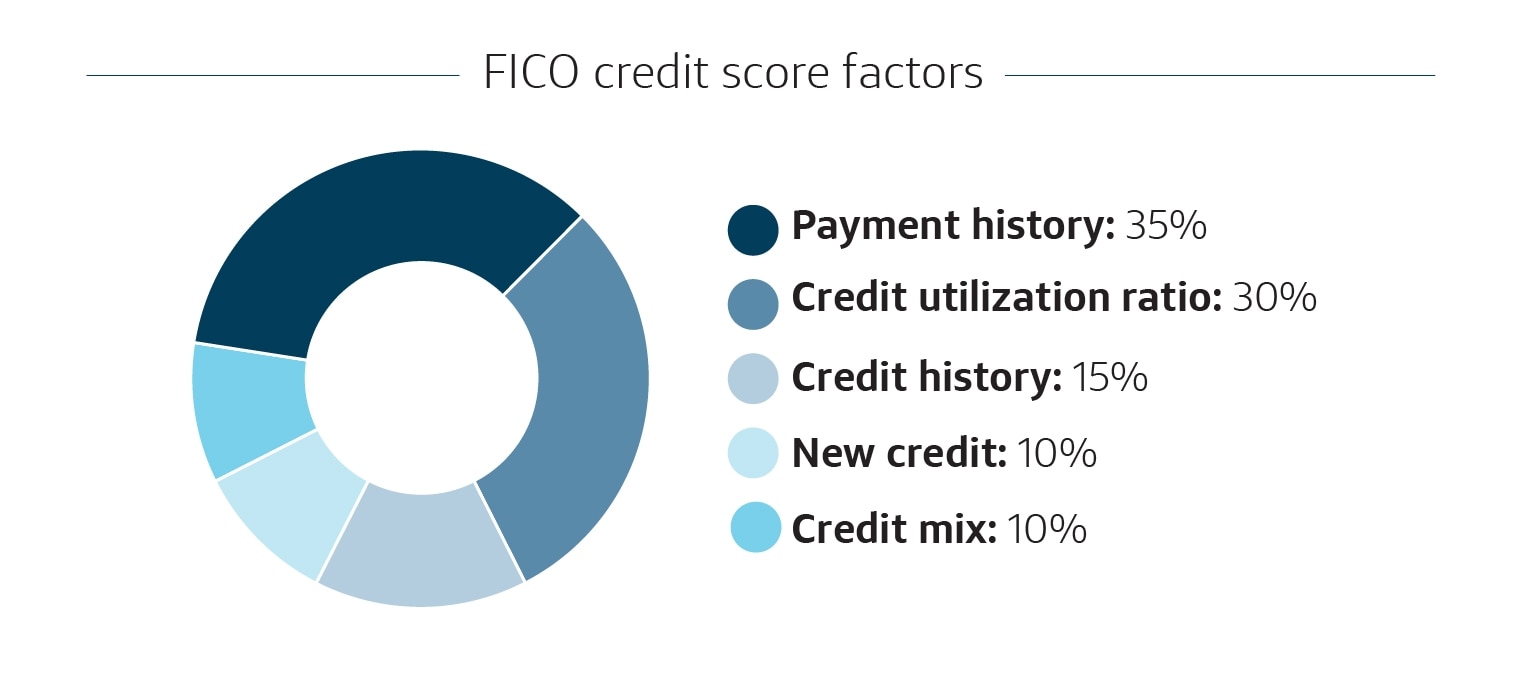

In general, FICO scores are calculated using five categories of credit data:

-

35% payment history

-

30% amount owed

-

15% length of credit history

-

10% credit mix

-

10% new credit

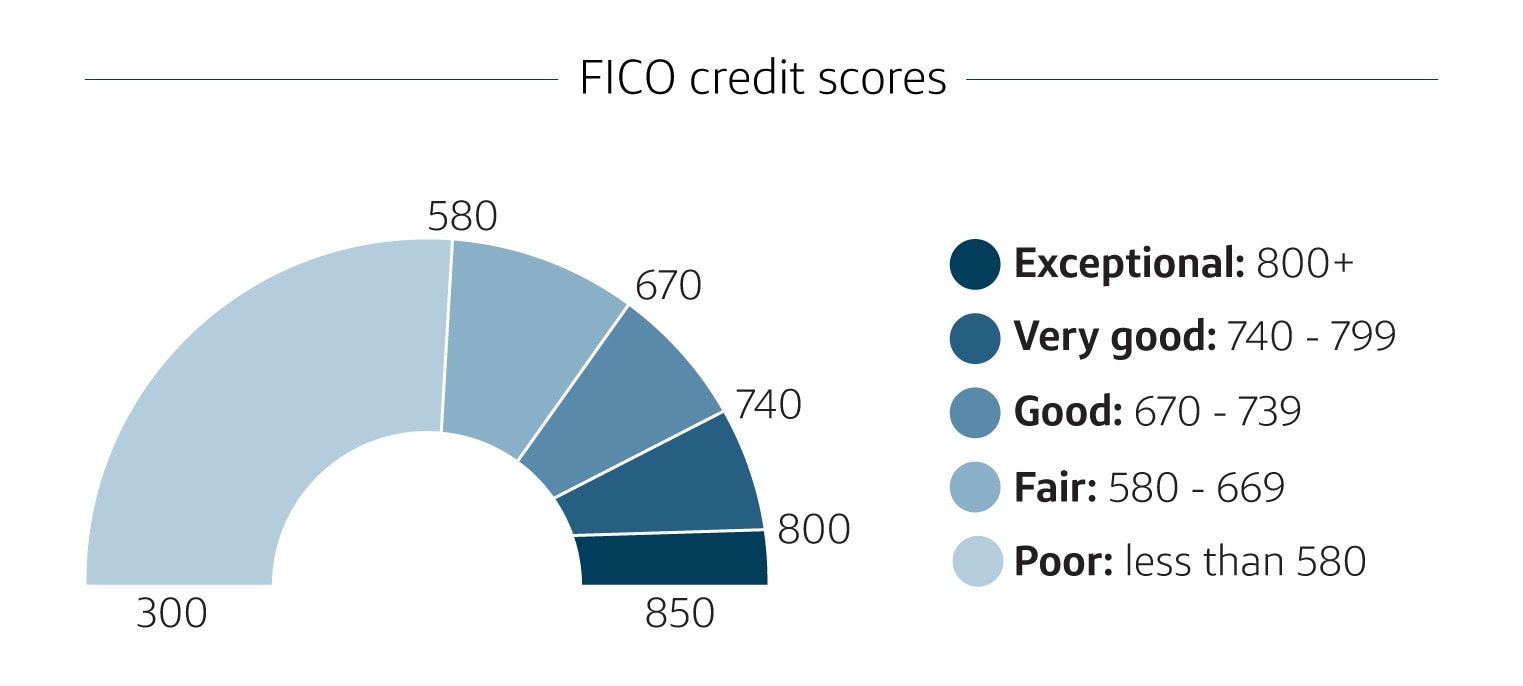

While scores range from 300 to 850, FICO says good credit scores fall between 670 and 739.

What is a VantageScore?

VantageScore was founded in 2006 by Equifax, Experian and TransUnion. The company uses several different formulas to calculate credit scores—including VantageScore 3.0 and VantageScore 4.0. Its scores are used by more than 3,400 financial institutions and eight of the 10 largest banks.

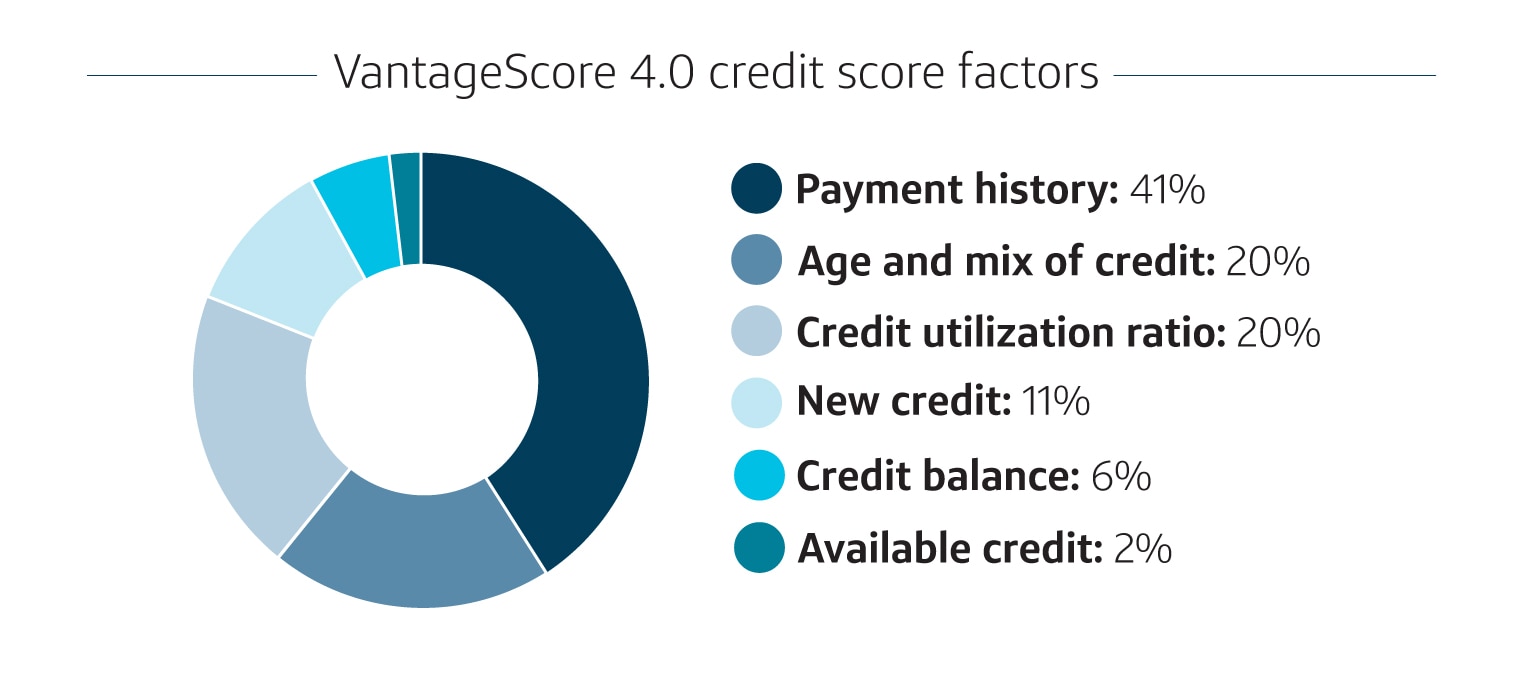

VantageScore has developed four credit-scoring models. The latest model, VantageScore 4.0, is calculated using the following credit behavior factors:

-

41% payment history

-

20% age and mix of credit

-

20% credit utilization ratio

-

11% new credit

-

6% credit balance

-

2% available credit

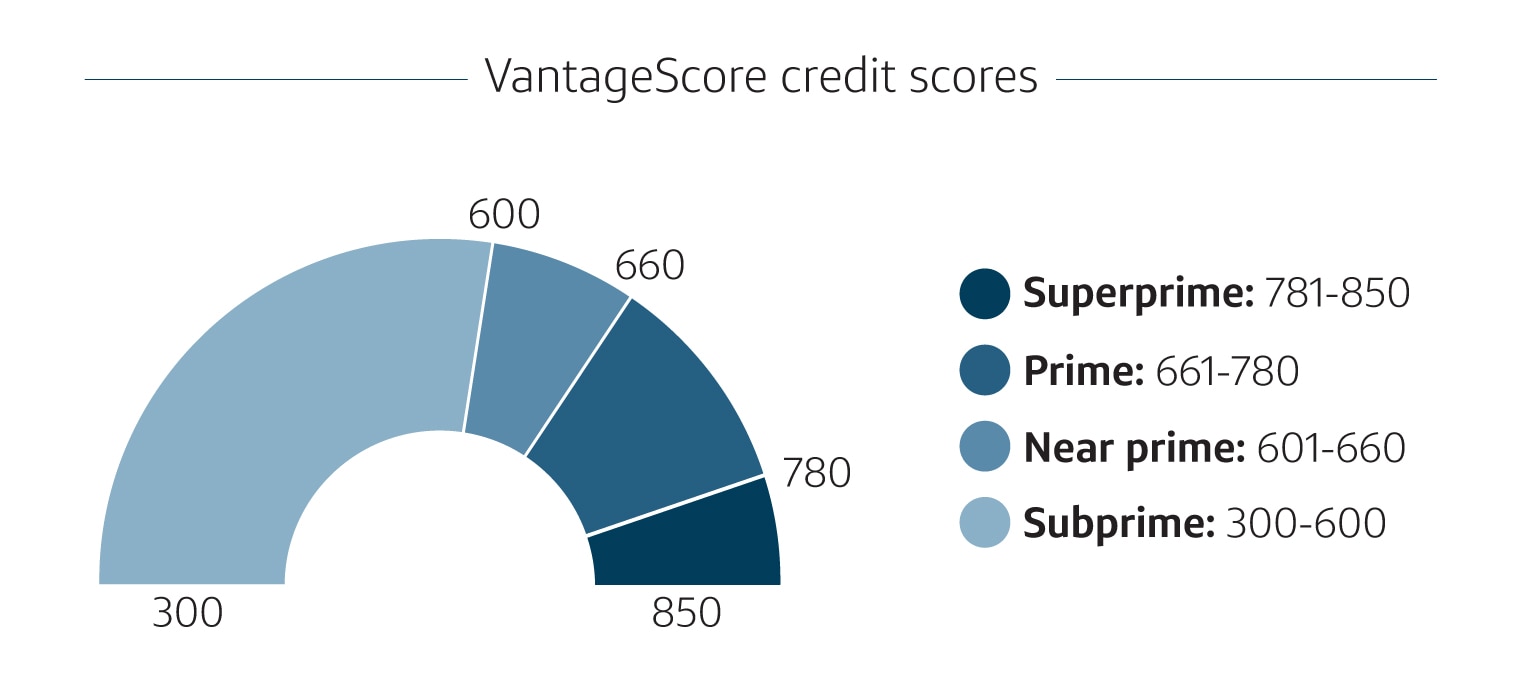

VantageScore 3.0 and 4.0 scores range from 300 to 850. And VantageScore says a score from 661 to 780 might be considered a good score.

How to check your credit score and credit report

CreditWise from Capital One helps make credit monitoring easy. CreditWise lets you monitor credit and keep up with changes. The CreditWise Simulator can even calculate how actions like paying down your balance or increasing your credit limit could affect your score.

You can also get free copies of your credit report from each of the three major credit bureaus by visiting AnnualCreditReport.com.

Monitoring your credit could help you avoid surprises next time you apply for a loan or credit card. And according to the CFPB, checking your own credit won’t hurt your scores.

Most accurate credit score FAQ

Here are the answers to some frequently asked questions about the most accurate credit score.

Which credit bureau is most accurate?

Similar to credit scores, there’s no single credit report that’s the most accurate. Lenders might report to all three major credit bureaus. Or they may only report to one or two. This means you might find slightly different information on each of your credit reports. But as long as there are no errors, one credit report isn’t more accurate than another.

What credit score do lenders use?

FICO scores are generally known to be the most widely used by lenders. While FICO Score 8 is the most common, mortgage lenders might use FICO Score 2, 4 or 5. Auto lenders often use one of the FICO Auto Scores. And credit card issuers may use the FICO Bankcard Scores.

VantageScore is also growing in popularity.

Which credit score is most important?

The most important credit score is situational and can change depending on what kind of credit you’re applying for. For example, if you’re applying for a mortgage, the lender may use an industry-specific version of your credit score. The same goes for applying for an auto loan or a credit card. Ultimately, decisions about credit applications are up to individual lenders.

Is the FICO score accurate?

FICO scores aren’t any more or less accurate than VantageScore credit scores. And remember, credit-scoring companies have multiple versions of scores.

Key takeaways: The most accurate credit score

When it comes to which credit score is most accurate, it might help to consider the factors that impact your scores—such as payment history and credit utilization. By focusing on your financial health and using credit responsibly, you can work to put yourself in a good position no matter which score a lender uses.

Ready to level up your credit? Check out these seven tips for how to improve your credit score.

Compare cards and explore digital features from Capital One

If you’re new to credit or searching for your next credit card, Capital One can help:

-

See if you’re pre-approved for credit cards without harming your credit scores.

-

If you’re looking to build your credit with responsible use, explore cards for people with fair credit.

-

Earn unlimited 1.5% cash back on every purchase every day with a cash back rewards card.

- Monitor your credit report and score with CreditWise from Capital One. It’s free for everyone, and using it won’t hurt your credit.